The Social Conglomerate

The Social Conglomerate

When news of the Facebook/WhatsApp deal broke, a lot of people gave me credit for being prescient : after all, I had just written 1,568 words on why messaging was mobile’s killer app . WhatsApp, though, was all but absent from the article, meriting but a single mention, and in parenthesis at that!

Viber does have strong user numbers, claiming 280 million registered users and 100 million monthly active users, and that is certainly a big part of the battle, but the creation of a meaningful platform is a significant next step that Viber (and WhatsApp) has not taken. A platform is about multi-sided markets; LINE and WeChat are so valuable because they not only have the users, but also advertisers, commerce sites, and developers.

Thus, while I’m skeptical of Rakuten and Viber, for LINE and WeChat the sky is the limit. Both have effectively built platforms on top of iOS and Android and smack dab in the middle of the most meaningful, and thus most-used, part of our lives: our communication and interaction with those we know and care about.

Thus the reason for the exclusion: I believe that business models matter, and while WhatsApp had the users, I’d heard enough about their (admirable!) principles to think they weren’t interested in either selling out or in building the sort of platform necessary to convert those users into a multi-billion dollar company.

I think that’s the first thing to understand about the $19 billion Facebook paid (including $3 billion in RSUs); WhatsApp as a standalone company, at least as presently constructed, with a miniscule staff and $1/user/year revenue model, was not worth anything close to $19 billion. But, that does not mean that Facebook overpaid.

Facebook Is Solely Focused on Attention, Not Monetization

There were two primary points I made in Messaging: Mobile’s Killer App :

- Messaging on mobile means constant communication with those closest to us. Those two words – constant, and closest – make it inevitable that messaging occupies more of a user’s attention than any other service.

- Messaging has a unique monetization model: platforms that combine direct marketing with immediate monetization opportunities

WhatsApp was hugely competitive when it came to the fight for user attention, but not really in the game when it came to platform-building; that’s why my post was mostly focused on LINE and WeChat: both have more potential as standalone companies than WhatsApp (not that Tencent would ever spin off WeChat!). Facebook, though, also doesn’t care about point number 2 – more about this in a moment – even as they care very deeply about point number 1, and from that perspective, WhatsApp is by far the most valuable of the messaging services. To put it another way, context matters: are you considering only messaging services, or are you considering the entirety of social?

Facebook is Building a Social Conglomerate

For several years Facebook-the-company sought to include the entirety of social interaction within Facebook-the-product. I tried to explain why this wasn’t possible last November in a post called The Multitudes of Social :

Last week Snapchat reportedly turned down a $3 billion dollar all-cash offer from Facebook. Apparently Facebook was worried about losing the teen demographic, or perhaps they were unnerved by the 350 million photos Snapchat claims to process per day. What seems clear, though, is that Facebook is intent on “owning social.”

The only problem with this strategy is that the very idea of owning social is a fool’s errand. To be social is to be human, and to be human is, as Whitman wrote, to contain multitudes. Multitudes of apps, in my case.

I obviously underestimated Mark Zuckerberg (I take solace in the fact I have lots of company on this point). While Zuckerberg may have given up on Facebook-the-product owning social, he remains determined that Facebook-the-company do just that. Thus the drive to release multiple standalone apps , and, more pertinently, the acquisition of first Instagram and now WhatsApp.

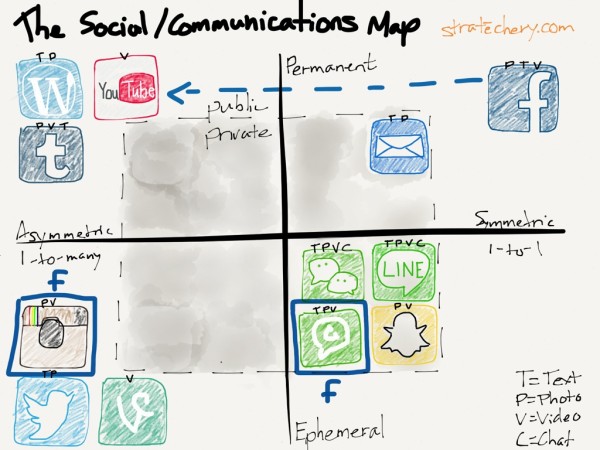

It was while writing The Multitudes of Social that I first created the Social/Communications Map; regular readers may be tired of it by now, but I think it’s essential to understanding what is happening:

{kind=link}

The big issue for Facebook-the-product is that while it has successfully extended itself into the public permanent broadcast segment (the blue dashed arrow), by doing so it has denied its brand permission to move into the private and ephemeral regions of the map. Facebook is irretrievably associated with content that you don’t want to risk haunting you in the future, and which you can never be sure is totally private. This was an acceptable tradeoff in the PC era; PCs are destination devices, and the relative effort it took to post pictures or status updates meant users were naturally inclined to put their best foot forward.

Mobile, though, because it is everywhere, captures far more human interaction; the majority of said interaction is ephemeral and private, and thus incompatible with what Facebook-the-product stood for. Facebook tried breaking in with products like Camera and Poke, but the Facebook association – and head start of competitors – was too much. And so, Facebook has bought its way in to the majority position in the category that dominates human interaction.

This is why I 100% believe Jan Koum when he says that WhatsApp will remain autonomous, at least from a product and branding perspective. To glom WhatsApp onto Facebook-the-product would be to throw away exactly what makes WhatsApp valuable to Facebook-the-company – that it’s not Facebook-the-product. It is better to think of Facebook-the-company as a conglomerate: Facebook-the-company builds, acquires, and manages multiple products that serve all the different segments of social. The largest and most well known product in their portfolio just happens to be called “Facebook” as well.

Facebook Doesn’t Need to Monetize WhatsApp

Describing Facebook-the-company as a conglomerate also explains the WhatsApp monetization riddle: namely, there is no need. The Facebook product division is absolutely crushing it and will make more than enough money with an excellent growth rate for many quarters to come. Moreover, its primary product – immersive display ads – are a perfect match for another company in the Facebook portfolio, Instagram, leaving WhatsApp free for the foreseeable future to asymmetrically compete 1 with LINE and WeChat for users in the private ephemeral space. I’d imagine the first step will be making WhatsApp completely free.

Even without immediate monetization, though, WhatsApp will provide immediate value to Facebook-the-company in two ways:

- As Facebook works to federate WhatsApp’s userbase with the Facebook userbase they will increasingly be able to harvest signal about users in a way that increases the value of Facebook-the-product’s display ad business.

- WhatsApp will provide great option value to FB the stock. Kakao is reportedly filing for a $2 billion IPO , and LINE is expected to do the same later this year for $10 billion ; investors will (rightly) presume that Facebook-the-company could similarly monetize WhatsApp if they chose to, increasing FB the stock’s upside.

The Messaging Space Going Forward

This deal is both good and bad news for the other messaging services. On the plus side, the eye-popping price should have a significant upward effect on the other messaging services’ valuations. On the other hand, WhatsApp now has significantly more resources, and, perhaps more importantly, significantly different incentives over the long run. Zuckerberg and company’s focus is not on building something sustainable, but rather on dominating the entire space.

That said, WhatsApp does not dominate everywhere, and its position in Asia in particular – especially the richer countries – has been a bit oversold :

- WeChat dominates China and is making inroads into Vietnam

- LINE dominates Japan, Taiwan and Thailand and is making inroads in Vietnam, Indonesia, Spain and Mexico

- Kakao dominates South Korea

In several of these countries WhatsApp was originally the leader, but the more full-featured competitors have since taken over. It will be interesting to see if Facebook responds by aping things like stickers, although a pure platform strategy along the lines of LINE seems less likely in the short-term.

One more note on messaging: it’s both more, and less, sticky than you might think. There are absolutely network effects at play: the best service is the one your friends are on. However, features like push notifications and badges makes it trivial to manage multiple networks; for example, most of my friends in Taiwan are on LINE, but it’s easy to respond to others who prefer WhatsApp, WeChat, Hangouts, or Facebook Messenger. I even make them share a badge!

Once again, it’s context that rules the day: different apps for different friends in different countries, but rarely multiple apps for the same groups and/or countries.

The Age of Conglomerates

This idea of conglomeration – ever larger companies, delivering ever more specialized and segmented products – isn’t limited to just Facebook. Google is arguably a machine-learning conglomerate with multiple products; Amazon a logistics conglomerate with multiple services; even Apple a personal computer conglomerate offering multiple products with different form factors and interaction models.

And, considering how computing power increases even as prices decrease, more specialized products that more perfectly fit different use cases is a natural result. So it is with Facebook-the-company: they are the social company, and no one can question their determination to offer a product that fits every use case, no matter the cost, and no matter the brand.

- Meaning, they don’t need to worry about monetization [ ↩ ]

文章版权归原作者所有。