PayPal’s Incentive Problem

PayPal’s Incentive Problem

Last week eBay announced that PayPal would be spun out into a separate company, fixing two big problems for PayPal:

- While PayPal grew big by being the payment method of choice for eBay transactions, 1 off-eBay transactions have since become the majority of PayPal’s revenue, meaning management’s need to prioritize eBay’s needs was misaligned with PayPal’s growth opportunities

- PayPal also had an individual-level incentive problem because they didn’t have their own stock. Stock options and/or grants are the incentive tool of choice for everyone from the CEO down to new hires in the tech industry, which meant any new PayPal hire was necessarily hitching their wagon to eBay

Still, I understood eBay’s previous argument that there were tremendous synergies between the businesses, and there’s no question that the loss of PayPal and the insight gained from being party to every transaction on the eBay marketplace is going to hurt the core business. Moreover, I think it’s highly likely that much of PayPal’s recent (impressive) growth was paid for with cash thrown off by eBay’s marketplace. There is a lot of logic to staying together.

That’s the thing with most big company endeavors, though: they almost always look good on paper. After all, the big company has all the cash, all the experience, all the developers that they can throw at any problem that arises. And yet, Silicon Valley is in many way premised on the idea that big companies can be beaten by, as the myth has it, a founder in a garage with little more than an idea. On paper it doesn’t make sense, and yet the examples are legion.

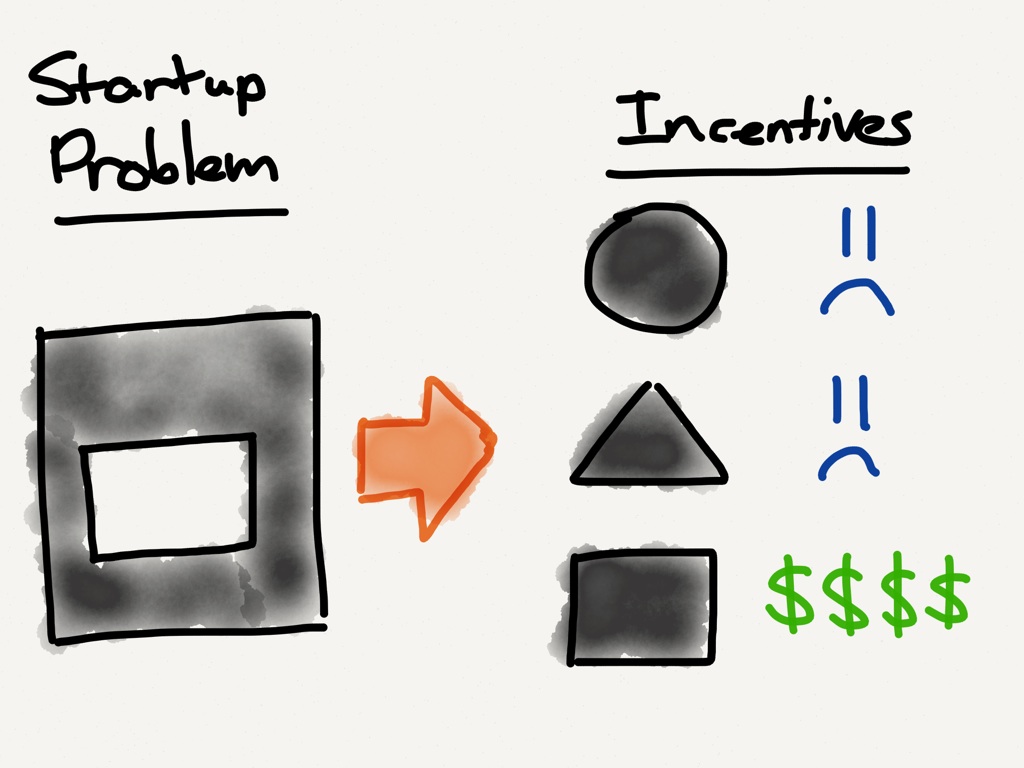

I’m not surprised though. Something I’ve learned over time – and believe today more strongly than I ever have – is that nothing matters more than incentives. It doesn’t matter how much money or experience or developers you have if your incentives are not aligned to solve the right problem. This is the big advantage that startups have vis a vis corporations: a startup starts with the problem and then creates the incentive structure under which their company operates. To put it another way, for a startup the incentives are defined by the problem. Small wonder, then, that startups are so focused on a solution.

A big company, on the other hand, has already solved a different problem – the problem that defined them back when they were as a startup. Now that the big company is facing a new problem, they have the wrong set of incentives – incentives that are defined by the old problem, not the new one.

This means that all of the advantages a big company has – their money, their experience, their developers – are all pointed in the wrong direction, leaving an opening for the new startup who has defined themselves by the new problem.

Unfortunately for PayPal and their future shareholders, PayPal is the old startup in this example. Their success in solving the “square” (peer-to-peer payments) problem has left them handicapped when it comes to the next “pentagon” opportunity: merchant-based payments, both online and off. eBay may be selling on top.

The central issue with peer-to-peer payments is that there is no merchant account involved. That means the entire infrastructure that has grown up around payments – particularly around credit cards – is not applicable. This infrastructure included fraud protection, authentication, dispute settling, and fees, lots of fees. PayPal built up something completely different: their primary connection was with your bank account, not your credit card, and instead of charging credit card-type fees, they simply kept your money a few days extras and profited off the float.

More broadly, the PayPal network – and the advantages that accrue to anyone who owns a network – was based on accounts with usernames and passwords. You couldn’t send money to someone – or more importantly, accept money – unless you had a PayPal account. In fact, many of PayPal’s legendary growth hacks, including literally paying people for signing up their friends, were predicated on increasing the number of user accounts on PayPal and thereby increasing the value of the network.

The problem for PayPal is that, as noted, peer-to-peer payments is a “square”-shaped problem; all of PayPal’s internal incentives are designed to solve this problem first-and-foremost. That’s why when it comes to a new problem, like easily enabling an individual or small business to be a merchant, PayPal is markedly inferior to what is on offer from startups like Stripe (for e-commerce) and Square (for offline purchases). For example, consider the purchase process on Stratechery :

- Stripe (my choice):

- Customer enters credit card right on the site

- Done!

- PayPal

- Customer is kicked out to a PayPal payment page

- Customer is asked to sign-in to PayPal, create an account, or proceed anonymously

- Should a customer sign in or create an account, they will be pushed to use a bank account to pay (the credit card option will be available but it’s purposely buried)

- Customer enters or selects a credit card on file

- Done!

The entire PayPal process is much more convoluted for users – I haven’t even gotten to how much more painful PayPal compared to Stripe is for merchants, but take my word that it’s even worse – and the reason has nothing to do with the transaction at hand; rather, pushing users to make accounts and to use their bank were keys to the old PayPal problem of enabling widespread peer-to-peer payments, and PayPal – like nearly all incumbents – can’t help but apply the old solution to the new problem even though it makes the new solution worse than it otherwise can be. And so Stripe is eating their lunch in the “pentagon”-shaped problem that is enabling someone like me to be a merchant. 2

PayPal’s offline challenges are much more basic: while PayPal was the first to allow individuals or small businesses to accept credit cards at all without a merchant account, physical retailers almost certainly already have a merchant account set up. This means that PayPal has to convert merchants from what most feel is a “good-enough” solution to one that, frankly, is only better because PayPal says it is. Sure, merchants like lower fees, but not necessarily the hassle of obtaining and training workers on new point-of-sale systems, and, even if they were to go through the trouble of supporting PayPal, what customer wants to unlock their phone, open an app, and enter a password when they can simply swipe a credit card? 3

And now, into the offline space comes Apple Pay, offering a payment experience that is far more secure and simple than anything that has come before. From an excellent write-up on the The Unofficial Apple Weblog about how Apple Pay security works:

With Apple Pay, no credit card data — even in encrypted form — is ever stored on the iPhone or on Apple’s servers. Similarly, no credit card data is ever transmitted to or stored on a merchant’s servers…the fundamental aspects of Apple Pay weren’t concocted in Cupertino. Rather, Apple Pay was designed in accordance with an emerging token-based mobile payments standard which aims to increase security and reduce the incidence of fraud. To that end, Apple is getting into the mobile payments space at just the right time. 4 So while Apple isn’t necessarily inventing the wheel here, Apple Pay again represents the first real implementation, on a massive scale no less, of the relatively fresh tokenization specification.

This is the tough part about being a tech company: PayPal spent years perfecting the perfect solution to that square-shaped hole that addressed thorny problems like identity, security, and fraud, and they were successful because we had nothing better. But time and technology move on, things like tokenization and NFC and Touch ID are invented, and new market opportunities predicated on the ease and ubiquity of credit cards but without the hassle and insecurity come along. And over there on the sideline is PayPal fixing a problem in a much smaller and ultimately less attractive market.

The analogy I would draw to PayPal today is Microsoft and mobile. I wrote in Microsoft’s Mobile Muddle :

Saying “Microsoft missed mobile” is a bit unfair; Windows Mobile came out way back in 2000, and the whole reason Google bought Android was the fear that Microsoft would dominate mobile the way they dominated the PC era. It turned out, though, that mobile devices, with their focus on touch, simplified interfaces, and ARM foundation, were nothing like PCs. Everyone had to start from scratch, and if starting from scratch, by definition Microsoft didn’t have any sort of built-in advantage. They were simply out-executed.

It’s actually more nefarious than that; it’s not only that Microsoft didn’t have any advantage in mobile relative to Apple or Google or anyone else, it’s that their previous success in a closely connected but ultimately different field put them at a significant disadvantage. Microsoft was (and in my opinion, continues to be ) heavily incentivized to approach the world with a PC mindset, but that’s the exact mindset they needed to let go of to build an effective mobile platform.

So it is with PayPal. Moving money between people who lack merchant accounts is an interesting problem that PayPal has mostly solved, but it turns out that this is a different problem than merchant account payment problems. Worse, it’s PayPal’s old solution – user accounts – that made them the least likely to come up with the new solution based on anonymous tokens, something that would have been true whether PayPal were a part of eBay or not. 5

In the long run PayPal will have a nice business with peer-to-peer transactions and, at least for the short term, moving money internationally (although this is clearly Bitcoin’s most obvious killer use case). However, the massive growth that awaits companies playing in the merchant space, including Apple, will always be just out of reach of a company willingly – and understandably – tying its own hands behind its back. 6

- I was on eBay from the beginning, which meant I was very familiar with getting money orders and sending them through the mail with faith the seller would come through. PayPal was a game-changer, their desperate efforts to diversify away from eBay notwithstanding [ ↩ ]

- Thus the acquisition of Braintree [ ↩ ]

- This is why PayPal was so slow to challenge Square; the sort of merchant who uses Square has no time for PayPal-style payments. They want to just deal with credit cards, which made the entire market less of a priority for PayPal [ ↩ ]

- Merchants also have an October 2015 deadline to update their terminals to support chip-and-pin; since new terminal will certainly include NFC, nearly all merchants will support NFC by next year [ ↩ ]

- I am aware that Apple Pay – and Stripe for that matter – are largely U.S. only affairs. I expect this situation will be fleeting, but even so, the U.S. is by far the largest payment opportunity in the world [ ↩ ]

- Yes, I have basically described disruption [ ↩ ]

文章版权归原作者所有。