TV Advertising’s Surprising Strength — And Inevitable Fall

TV Advertising’s Surprising Strength — And Inevitable Fall

It’s been a good few months for TV executives, who are in the middle of upfront negotiations with advertisers for the 2016-2017 television season. Variety reports :

After several years of moving money out of TV ad budgets to experiment with new digital outlets and social media, several big advertisers are spending more on the boob tube – and the result, according to ad buyers and other executives familiar with the pace of this year’s “upfront” negotiations, are a series of rate increases that TV has not won since the end of the last U.S. recession.

“It’s all about money coming back into the marketplace,” said one media buying executive, noting that consumer packaged goods companies, quick-service restaurant chains and pharmaceutical companies are moving money into TV’s annual upfront market, when the nation’s big media companies try to sell the bulk of their ad inventory for the coming programming cycle. Some of the money is coming back from digital spending, and some of it is being moved from TV’s so-called “scatter” market, when advertisers pay for commercials much closer to their air date.

Reports indicate those rate increases are running between 7% and 12% , and follow on a 2015-2016 season that saw scatter advertising — advertising purchased closer to the airing date — up 16% year-over-year . Apparently all that digital advertising hype was just a fad, right?

I wouldn’t be so sure.

Advertising and Attention

Despite all of the upheaval caused by the Internet, there are two truths about advertising that have remained constant:

- Advertising’s share of GDP has remained consistent for 100 years 1

- TV’s share of advertising, after growing for 40 years, has also remained consistent at just over 40% for the last 20 years

Those twenty years have seen the emergence of digital advertising generally, and, over the last five years, mobile advertising: while this emergence is likely responsible for the halt in growth for TV, the real victims have been radio, magazines, and especially newspapers, which have shrunk from a nearly 40% advertising share to about 10%.

Still, digital and mobile’s 33% share of advertising falls well short of the amount of attention attracted. Digital accounted for 47% of time spent with media in 2015, up from 32% in 2011, while TV has fallen from 41% in 2011 to 35% in 2015. 2 This decline, though, is not evenly distributed: this jarring chart from Redef about the change in hours spent watching TV by age group shows that the situation for TV is much worse than the top-line numbers suggest:

The three age groups with the biggest declines — millennials, basically — are the most attractive to the brand advertisers that dominate TV advertising: for one, the younger you are the less likely you are to have developed affinity for a particular brand, and for another, the younger you are the more years a brand has to earn back the money spent building said affinity. Small wonder brands have been so eager to jump on new digital platforms where said millennials are actually spending their time.

So why is money suddenly flowing back to TV?

The Relationship Between TV and Advertisers

The most obvious reason for TV’s enduring appeal to advertisers is that it is a pretty fantastic advertising medium: relaxed viewers, immersive experience, etc. The appeal, though, goes deeper: the very institution of television advertising is intertwined with the kinds of advertisers that use it the most, the products they sell, and the way they are bought-and-sold. And what should be terrifying to television executives is that all of those pieces that make television advertising the gold mine that it has been are under the exact same threat that TV watching itself is: the threat of the Internet.

Start with the top 25 advertisers in the U.S. The list is made up of:

- 4 telecom companies (AT&T, Comcast, Verizon, Softbank/Sprint)

- 4 automobile companies (General Motors, Ford, Fiat Chrysler, Toyota)

- 4 credit card companies (America Express, JPMorgan Chase, Bank of America, Capital One)

- 3 consumer packaged goods (CPG) companies (Procter & Gamble, L’Oréal, Johnson & Johnson)

- 3 entertainment companies (Disney, Time Warner, 21st Century Fox)

- 3 retailers (Walmart, Target, Macy’s)

- 1 from electronics (Samsung), pharmaceuticals (Pfizer), and beer (Anheuser-Busch InBev)

Notice that the vast majority of the industries on on this list are dominated by massive companies that compete on scale and distribution. CPG is the perfect example: building a “house of brands” allows a company like Procter & Gamble to target demographic groups even as they leverage scale to invest in R&D, bring down the cost of products, and most importantly, dominate the distribution channel (i.e. retail shelf space). Said retailers, meanwhile, are huge in their own right, not only so they can match their massive suppliers at the bargaining table but also so they can scale logistics, inventory management, store development, etc. Automobile companies, meanwhile, are not unlike CPG companies: they operate a “house of brands” to serve different demographics while benefitting from scale in production and distribution; the primary difference is that they make money through one large purchase instead of over many smaller purchases over time.

Similar principles apply to the other companies on this list: all are looking to reach as many consumers as possible with blunt targeting at best, all benefit from scale, and all are looking to earn significant lifetime value from consumers. And, along those lines, all can afford the expense of TV. In fact, the top 200 advertisers in the U.S. love TV so much that they make up 80% of television advertising, despite accounting for only 51% of total advertising (and 41% of digital).

Note, though, that many of the companies on this list are threatened by the Internet:

- CPG companies are threatened on two fronts: on the high end the combination of e-commerce plus highly-targeted and highly-measurable Facebook advertising have given rise to an increasing number of boutique CPG brands that deliver superior products to very targeted groups. On the low end, meanwhile, e-commerce not only reduces the shelf-space advantage but Amazon in particular is moving into private label in a big way.

- Relatedly, big box retailers that offer few advantages beyond availability and low prices are being outdone by Amazon on both counts . In the very long run it is hard to see why they will continue to exist.

- The automobile companies, meanwhile, are facing three separate challenges : electrification, transportation-as-a-service (i.e. Uber), and self-driving cars. The latter two in particular (and also the first to an extent) point to a world where cars are pure commodities bought by fleets, rendering advertising unnecessary.

The other companies face less of a long-term threat, some because they are already commoditized — telecoms, credit cards, electronics — and others because they will probably grow: big movies are only getting bigger (entertainment), and the population is getting older (pharmaceuticals). Still, the inescapable reality is that TV advertisers are 20th century companies: built for mass markets, not niches, for brick-and-mortar retailers, not e-commerce. These companies were built on TV, and TV was built on their advertisements, and while they are propping each other up for now, the decline of one will hasten the decline of the other.

TV Advertising’s Dead Cat Bounce

I also suspect the nature of the biggest TV advertisers explains TV’s dead cat bounce: brands uniquely suited to TV are probably by definition less suited to digital advertising, which at least to date has worked much better for direct response marketing. No one is going to click a link in their feed to buy a car or laundry detergent, and a brick-and-mortar retailer doesn’t want to encourage shopping to someone already online. So after a bit of experimentation, they’re back with TV.

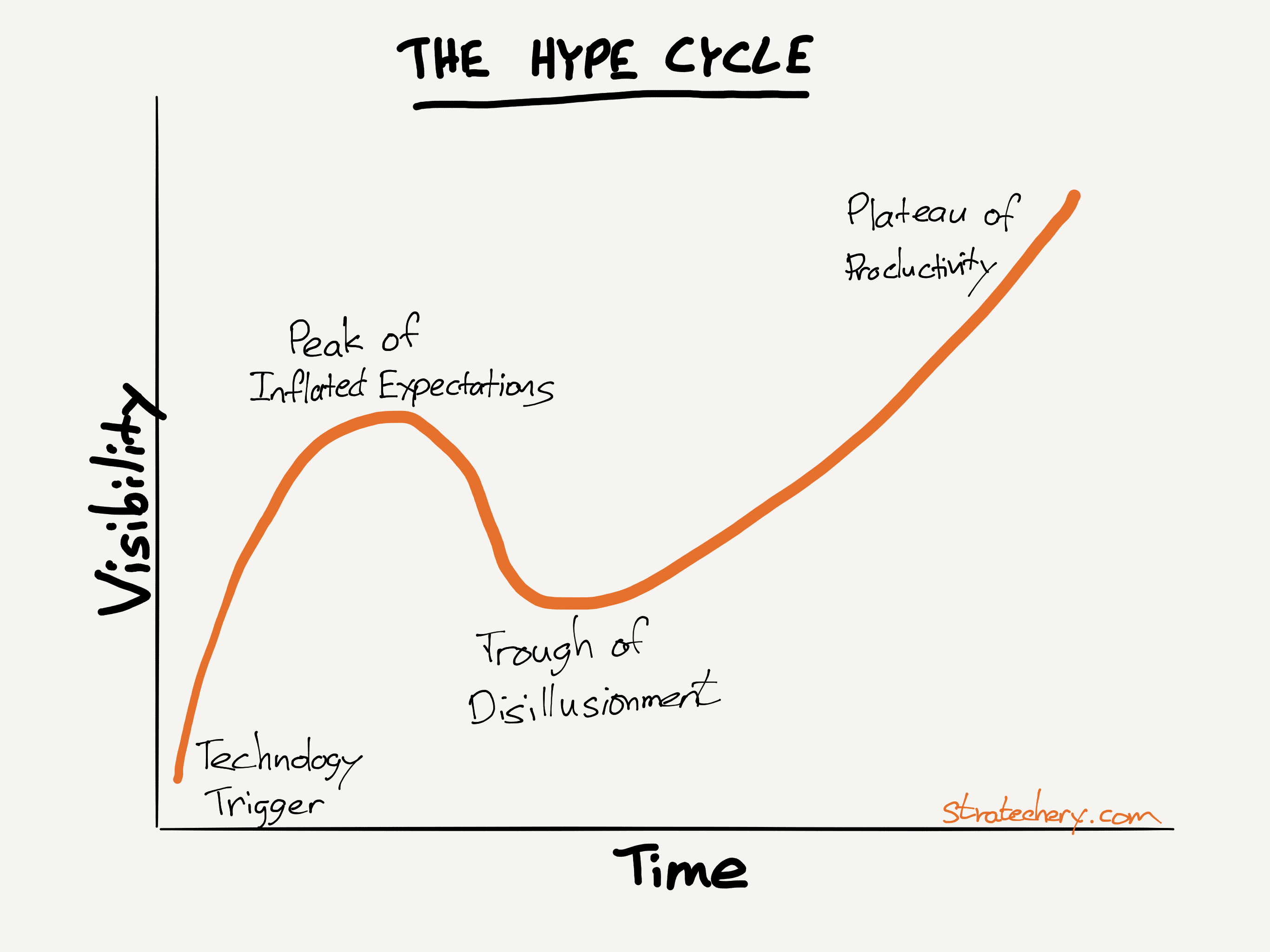

Still, I think Facebook and Snapchat in particular will figure brand advertising out: both have incredibly immersive advertising formats, and both are investing in ways to bring direct response-style tracking to brand advertising, including tracking visits to brick-and-mortar retailers . It wouldn’t surprise me if brand advertising on digital is following the hype cycle:

This is the story of most things Internet-related, not just narrowly but broadly: it’s no accident many of today’s startups are repeating ideas from the dot com era ; it’s not that they were wrong but that they were too early. And, when it comes to old world companies, if you turn that graph upside down, the “trough of disillusionment” looks a lot like a bounce-back!

Ultimately, given the shift in attention, the threats faced by their best advertisers, and the oncoming train that is Facebook and Snapchat, were I a TV executive I wouldn’t get too excited about one nice week of ad sales. Indeed, the industry has been shifting to subscriptions for years , and while advertising will hold up for a while, the big drama is who will be left without a chair when the music stops. 3

Coda: Aggregation Theory

One more thing: I wrote a piece earlier this year called The Fang Playbook that posited that Facebook, Amazon, Netflix, and Google (plus Uber) were structurally very similar companies: all leveraged zero distribution costs and zero transaction costs to own users at scale via a superior experience that commoditized suppliers and let them skim off the middle, either through fees, subscriptions, or ads. 4

What I described above is the opposite side of the coin: linear television and its advertisers were all predicated on owning distribution and thus owning customers. The Internet has or is in the process of destroying their business models for broadly similar reasons; for now the intertwinement of these models is keeping everyone afloat, but that only means that when the end comes it will come more swiftly and broadly than anyone is expecting.

- Although this may be slowing ; more on this tomorrow [ ↩ ]

- Note that the advertising-free Netflix is categorized as digital; although the streaming service still serves a minority of U.S. households, its subscribers watch an average of 1 hour and 33 minutes a day, and are responsible for a good deal of TV’s fall-off. [ ↩ ]

- Viacom, for example [ ↩ ]

- Aka Aggregation Theory [ ↩ ]

文章版权归原作者所有。