Stitch Fix and the Senate

Stitch Fix and the Senate

There was an interesting line of commentary around the news that Stitch Fix, the personalized clothing e-commerce company, was going to IPO: these numbers are incredible ! Take this article in TechCrunch as an example ( emphasis mine ):

Stitch Fix has filed to go public, finally revealing the financial guts of the startup which will be a test of modern e-commerce businesses that are looking to hit the market — and the numbers look pretty great!

Let’s start off really quick with profits: aside from the last two quarters, Stitch Fix posted a six-quarter streak of positive net income. We talk a lot about companies that are planning to go public that show pretty consistent (or even increasing) losses, but Stitch Fix looks like a company that has actually managed to build a healthy business . The company finally lost money in the last two quarters, but even then, its losses decreased quarter-over-quarter — with the company only losing around $4.5 million in the second quarter this year.

Compare this to the TechCrunch article written when Box, a company that ultimately IPO’d at a similar market-cap as Stitch Fix will (~$2 billion), first filed its IPO:

Box has long been rumored to have quickly growing revenues and large losses, which has proven to be the case. For the full-year period that ended January 2014, Box’s revenues grew to $124 million, up from $58.8 million the year prior. However, the company’s net loss also expanded in the period, with Box posting losses of $168 million for the full-year period that ended January 2014, more than its total top line for the period. In the period prior, Box lost a more modest $112 million.

What is driving Box’s yawning losses? Sales and marketing. The company’s line item for those expenses expanded from $99.2 million for the year ending January 2013, to $171 million for the year ending January 31, 2014. That was the lion’s share of Box’s $100 million increasing in operating costs during the period. Or, put more simply, Box spent more dollars on selling its products in the year than it brought in revenue during the period. This could indicate customer churn, or merely a tough market for cloud products.

In fact, both explanations were completely wrong: Box’s losses were due to the company investing in future growth; a detailed look at cohorts revealed that Box was increasing profitability over time because churn was negative (because existing customers were increasing spend by more than the revenue lost by those leaving), and the share of cloud spending amongst enterprise broadly is only going in one direction — up. To that end, investing more in future growth — even though it made the company unprofitable in the short-term — was an obviously correct decision.

Stitch Fix Concerns

To that end, I find Stitch Fix’s number more concerning than I did Box’s:

- First, the average revenue per client has decreased over time: according to the numbers provided in Stitch Fix’s S-1 , the average client in 2016 generated $335 in revenue in the first six months, and $489 in revenue for the first 12 months; there is not a comparable set of numbers for earlier cohorts (itself a red flag), but the average 2015 client generated $718 in revenue over two years. To the extent these cohorts can be compared, that means $335 in the first six months, $154 in the second six months, and an average of $115 in the third and fourth six-month periods.

- Second, these clients are increasingly expensive to acquire. Stitch Fix increased its ‘Selling, General and Administrative Expenses’ by 56% last year, but revenue increased by only 34%; advertising spend specifically increased from $25.0 million to $70.5 million (182%), vastly outpacing revenue growth.

- Third, revenue growth is slowing substantially, despite the fact Stitch Fix has expanded its product offerings, both within its core women’s market as well as expansions to Petite, Maternity, Men’s, and Plus apparel. I noted last year’s revenue growth was 34%; the previous year’s growth was 113%, and the year before that 368%.

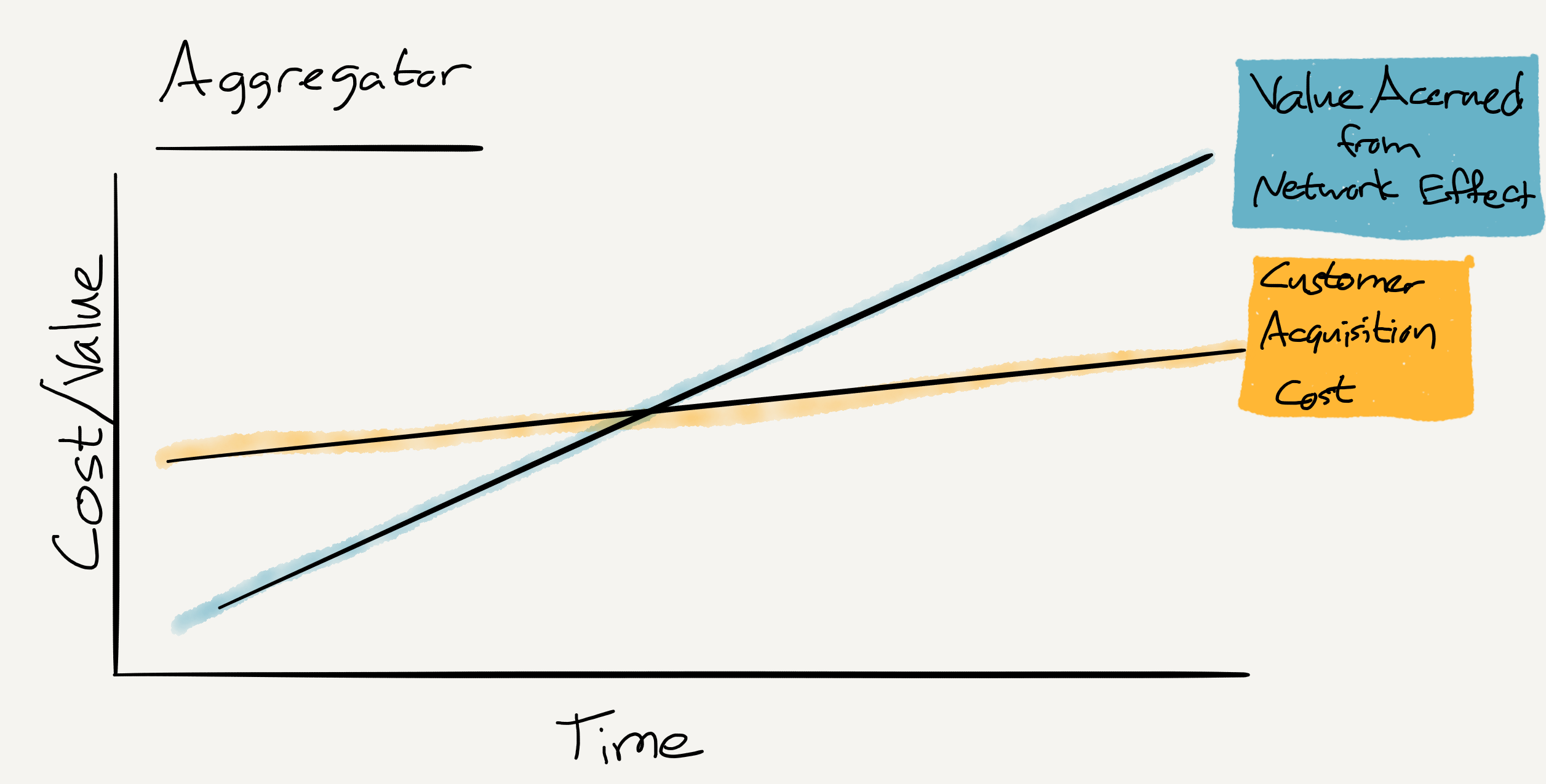

The problem for Stitch Fix is the same bugaboo encountered by the majority of consumer companies: the lack of a scalable advantage in customer acquisition costs. I wrote about this earlier this year in the context of Uber :

Uber’s strength — and its sky-high valuation — comes from the company’s ability to acquire customers cheaply thanks to a combination of the service’s usefulness and the effects of aggregation theory : as the company acquires users (and as users increases their usage) Uber attracts more drivers, which makes the service better, which makes it easier to acquire marginal users (not by lowering the price but rather by offering a better service for the same price). The single biggest factor that differentiates multi-billion dollar companies is a scalable advantage in customer acquisition costs; Uber has that.

On the other hand, it seems likely Stitch Fix does not, even though the company did argue in its S-1 that it benefited from network effects:

We believe we are the only company that has successfully combined rich client data with detailed merchandise data to provide a personalized shopping experience for consumers. Clients directly provide us with meaningful data about themselves, such as style, size, fit and price preferences, when they complete their initial style profile and provide additional rich data about themselves and the merchandise they receive through the feedback they provide after receiving a Fix. Our clients are motivated to provide us with this detailed information because they recognize that doing so will result in a more personalized and successful experience. This perpetual feedback loop drives important network effects, as our client-provided data informs not only our personalization capabilities for the specific client, but also helps us better serve other clients.

This may be true — it makes sense that it would be — but while it may help Stitch Fix better serve new customers it is not clear how it helps the company acquire said customers in the first place. Instead, like most consumer companies, it seems likely that Stitch Fix leveraged word-of-mouth to own its core market of women who value convenience in shopping for clothing, but struggled to break beyond that segment — and to the extent it did, found consumers who spend less and churn more. In other words, unlike successful aggregators, the improvement generated by the network effect, such that it was, was less than the increase in acquisition cost:

The key to truly break-out consumer companies is having these lines reversed: the network should be generating an improvement in benefits that exceeds the cost of acquiring customers, fueling a virtuous cycle.

Stitch Fix’s Success

That said, I fully expect Stitch Fix’s IPO to be successful: how could it not be? In stark contrast to many would-be aggregators, Stitch Fix has taken a shockingly small amount of venture capital — only $42.5 million . Instead the company has been profitable — on an absolute basis in 2015-2016, and quite clearly on a unit basis (including acquisition costs) throughout — and cash flow positive. That increased marketing expenditure is being paid by current customers, not venture capitalists. To that end, a $2 billion IPO would be a massive win for Stitch Fix’s investors and Katrina Lake, the founder.

Moreover, while Stitch Fix’s growth may be slowing, that is by no means fatal: the company is a perfectly valid business to own exactly as it is. Indeed, I am in fact deeply impressed by Stitch Fix: it seems quite clear that early on Lake realized that the company was not an aggregator , which meant building a business, well, normally. That means making real profits, particularly on a unit basis. Even then, though, the company was clearly worthy of venture capital: Baseline Ventures and Benchmark will see a 10x+ return.

To that end, Stitch Fix is a more important company than it may seem at first glance: it proves there is a way to build a venture capital-backed company that is not an aggregator, but still a generator of outsized returns. The keys, though, are positive unit economics from the get-go, and careful attention to profitability. The reason this matters is that these sorts of companies are by far the more likely to be built: Google and Facebook are dominating digital advertising, Amazon is dominating undifferentiated e-commerce, Microsoft and Amazon are dominating enterprise, and Apple is dominating devices. To compete with any of them is an incredibly difficult proposition; better to build a real differentiated business from the get-go, and that is exactly what Stitch Fix did.

RSUs, Options, and Taxes

The other winners in Stitch Fix’s IPO are all of its employees that hold stock options and restricted stock units (RSUs): they too have benefited from the company’s reticence in raising money; those options and RSUs are priced significantly below the company’s IPO price. And, when that IPO happens later this week, said employees will benefit tremendously — rightly alongside the IRS. When the IPO happens those stock options and RSUs will become taxable, and the majority of Stitch Fix employees will have to sell some portion of their holdings to cover their bill. This is entirely reasonable: they will have earned their reward for building Stitch Fix into the impressive company it has become, and they will pay taxes on that reward.

What would not have been reasonable, though, would have been to pay those taxes before the IPO. After all, when Stitch Fix started it was not at all certain the company would reach this milestone: there are a whole host of companies that raised far more than Stitch Fix’s $42.5 million that ended up going out of business, or being sold off as an acquihire such that employees earned nothing.

Indeed, I suspect that startup employees are, on balance, terribly underpaid: most take on jobs with lower salaries relative to established companies simply for the chance of making an outsized return should the company they work for IPO; the odds of that happening mean the expected value of the options and RSUs they receive are quite low.

To that end, it is tempting to be skeptical about venture capital protestations about a Senate tax provision that would tax stock options and RSUs at the moment they vest ; given the uncertain value, any startup seeking to attract employees would have to significantly up their cash compensation, which would be better for most employees (and thus worse for most venture capitalists) — in the short term, anyways.

The Startup Ecosystem

The problem with this point of view is that the startup employee frame is much too narrow: leaving aside the fact than anyone qualified to work at a startup is already far better off than nearly everyone on earth, the broader issue is that the scope for building successful venture-backed companies is narrowing.

Stitch Fix is a perfect example: I just explained that the company has uncertain growth prospects, but is still a big success thanks in large part to its disciplined approach to the bottom line. That should be a model for more companies: quickly determine if your business can be an aggregator with the scalable acquisition cost advantages that come with it, and if not, build a sustainable business sooner rather than later. That will allow everyone to benefit: founders, venture capitalists, employees, and most importantly, consumers.

A disciplined approach to the bottom line, though, means taking full advantage of a start-up’s number one recruiting tool: stock options and RSUs, in lieu of fully competitive salaries. Had Stitch Fix had to pay its employees in cash the company would have likely had to raise more money, reducing the likelihood of a successful outcome for everyone — including the IRS.

The downside, though, is even more acute for the companies that might seek to become aggregators themselves and so challenge companies like Google, Facebook, or Amazon directly. Any such would-be disruptor — and keep in mind, disruption is the only means by which these companies might ever be threatened — would need to raise huge amounts of capital, likely over an extended period of time. Moreover, the odds of success would be commensurately lower, making it even more likely associated stock options and RSUs might be worthless. To that end, taxing said options and RSUs would make start-up jobs even less attractive, and any sort of alternative — including increased cash compensation — would not only reduce the likelihood of startup success but also deny employees the chance to share in a successful outcome.

Tech’s Constituencies

Like most commentators, I am often guilty of lumping all of technology into one broad bucket; that makes sense when considering the impact of technology on society broadly. This tax bill, though, is a reminder that tech has two distinct constituencies with concerns that don’t always align:

- Incumbents have successful business models that throw off oodles of cash; their concern is about protecting those models, and they will spend to do so

- Venture capitalists and founders are seeking to build new businesses that, more often than not, threaten those incumbents; their edge is the opportunity to build businesses perfectly aligned to the problem they are seeking to solve

Tech employees get different benefits from each camp: the former provides high salaries and great perks; you can have a very nice life working for Facebook or Google. Startups, on the other hand, offer a chance to own a (small) piece of something substantial, at the cost of short-term salary — and that is worth preserving. Not only is it important to offer an accessible route up the economic ladder, former startup employees are a key part of the Silicon Valley ecosystem, often providing the initial funding for other new companies.

To that end, what is critical to understand about this proposed tax change is that incumbent companies won’t be hurt at all: sure, they may have to change their compensation to be more cash-rich and RSU-light, but cash isn’t really a constraint on their business. Higher salaries are a small price to pay if it means startups that might challenge them are handicapped; small wonder none of the big companies are lobbying against this provision.

Towards a Startup Lobby

This isn’t the first time the needs of the big tech companies has diverged from startups: net neutrality, for example, is much more important if you don’t have the means to pay to play. The same thing applies to tax laws more broadly, including corporate tax reform and offshore holdings.

Perhaps the most clear example, though, is antitrust: the companies that are hurt the most by Google, Facebook, and Amazon dominance are not analog publishers or retailers, but more direct competitors for digital advertising or e-commerce — mostly startups. Nearly all of the lobbying about this issue, though, is funded by the incumbents, for all of the reasons noted above: they have cash to burn, and business models to protect.

To that end it might behoove the startup community — and to be more specific, venture capitalists — to start building a counterweight. I am optimistic this Senate provision will ultimately be stripped from the proposed tax bill, but that the very foundation of startup compensation was so suddenly threatened should serve as a wake-up call that depending on Google or Apple largesse to represent the tech industry is ultimately self-defeating.

文章版权归原作者所有。