Disney and Fox

Disney and Fox

It’s always a risk writing about a deal before it is official: CNBC reported a month ago that Disney was in talks to acquire many of 21st Century Fox’s assets, including its eponymous movie studio, TV production company, cable channels, and international assets (but not the Fox broadcast network, Fox News, FS1 — Fox’s sports channel — and Fox Business). All was quiet until last week, when CNBC again reported that the deal was on, and now included 21st Century Fox’s Regional Sports Networks.

As I write this it is now widely reported that the deal is imminent; most notably, Comcast has dropped out of the bidding, which means the only question is whether or not Disney can close the deal: they would be crazy not to.

The Logic of Acquisition

The standard reason given for most acquisitions is so-called “synergy”: the idea that the two firms together can generate more revenue with lower costs than they could independently; most managers point towards the second half of that equation, promising investors significant cuts through reducing the number of workers doing the same thing. Certainly that is an argument in Disney’s favor: nearly everything 21st Century Fox does Disney does as well.

Still, it’s not exactly a convincing argument; acquisitions also incur significant costs: the price of the acquired asset includes a premium that usually more than covers whatever cost savings might result, and there are significant additional costs that come from integrating two different companies. Absent additional justification, the cost-savings argument comes across as justification for management empire-building, not value creation.

That’s not always the reason though: the cost-savings argument is often a fig-leaf for an acquisition that reduces competition; better for management to claim synergies in costs than synergies that result in cornering a market. The result is managers who routinely make weak arguments in public and strong arguments in the boardroom.

The best sort of acquisitions, though, are best described by the famous Wayne Gretzky admonition, “Skate to where the puck is going, not where it has been”; these are acquisitions that don’t necessarily make perfect sense in the present but place the acquirer in a far better position going forward: think Google and YouTube, Facebook and Instagram, or Disney’s own acquisition of Capital Cities (which included ESPN).

What makes this potential acquisition so intriguing is that it is a mixture of all three — and which of the three you pick depends on the time frame within which you view the deal.

The Not-so-distant Past

Go back to that Capital Cities acquisition: the 1995 deal was, at the time, the second largest acquisition ever, and it primed Disney to dominate the burgeoning cable television era.

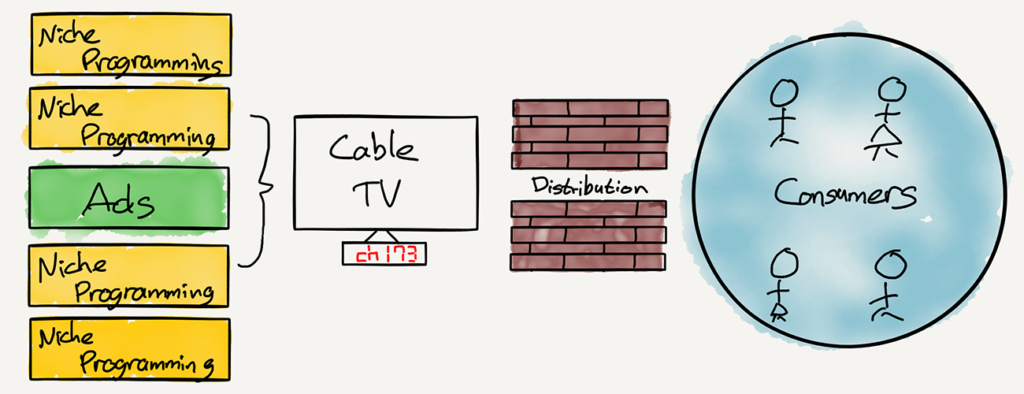

I sketched out the structure of cable TV earlier this year in The Great Unbundling :

The key takeaway should be a familiar one: economic power came from controlling distribution. The cable line was the only way for consumers to obtain the fullest possible array of in-home entertainment, which meant that distributors were able to charge consumers as much as they could bear.

The real negotiations in this value chain took place between content producers and distributors, which ultimately determined who made the most profit, and here Capital Cities + Disney was a powerful combination:

- First and foremost, ESPN was well on the way to establishing itself as the most indispensable cable channel amongst consumers, allowing it to command carriage fees that were multiples higher than any other channel.

- Secondly, Disney was able feed content to ABC just in time for the FCC having loosened regulations on broadcast networks producing their own content (instead of acquiring it).

- Third, Disney built a bundle within the bundle: distributors had to not only pay for ESPN, but also for the Disney channel, A&E, Lifetime, and the host of spinoff channels that followed; any proper accounting for ESPN’s ultimate contribution to Disney’s bottom line should include the above-average carriage fees charged by all of Disney’s properties.

This all seems obvious in retrospect, but at the time most of the attention was on ABC, then the most-profitable broadcast channel. The puck, though, was already moving towards cable.

The Fading Present

The dominant story in media over the last few years has been the slow-but-steady breakdown of that cable TV model. In August 2015, now-Disney CEO Bob Iger — who joined the company in that Capital Cities deal — admitted on an earnings call that ESPN and the company’s other networks, which had previously generated 45% of Disney’s revenue and 68% of its profit, were losing customers:

We are realists about the business and about the impact technology has had on how product is distributed, marketed and consumed. We are also quite mindful of potential trends among younger audiences, in particular many of whom consume television in very different ways than the generations before them. Economics have also played a part in change and both cost and value are under a consumer microscope. All of this has and will continue to put pressure on the multichannel ecosystem, which has seen a decline in overall households as well as growth in so-called skinny or cable light packages.

In fact, as I detailed earlier this year , Disney had not been realistic at all about the “impact technology [had] had on how product is distributed, marketed and consumed”:

Back in 2012 the media company signed a deal with Netflix to stream many of the media conglomerate’s most popular titles…Iger’s excitement was straight out of the cable playbook: as long as Disney produced differentiated content, it could depend on distributors to do the hard work of getting customers to pay for it. That there was a new distributor in town with a new delivery method only mattered to Disney insomuch as it was another opportunity to monetize its content.

The problem now is obvious: Netflix wasn’t simply a customer for Disney’s content, the company was also a competitor for Disney’s far more important and lucrative customer — cable TV. And, over the next five years, as more and more cable TV customers either cut the cord or, more critically, never got cable in the first place, happy to let Netflix fulfill their TV needs, Disney was facing declines in a business it assumed would grow forever.

That business was predicated on cable’s monopoly on in-home entertainment; what Netflix offered was an alternative:

Netflix’s path to a full-blown cable TV competitor is one of the canonical examples of a ladder strategy :

Netflix started by using content that was freely available (DVDs) to offer a benefit — no due dates and a massive selection — that was orthogonal to the established incumbent (Blockbuster). This built up Netflix’s user base, brand recognition, and pocketbook

Netflix then leveraged their user base and pocketbook to acquire streaming rights in the service of a model that was, again, orthogonal to incumbents (linear television networks). This expanded Netflix’s user base, transformed their brand, and continued to increase their buying power

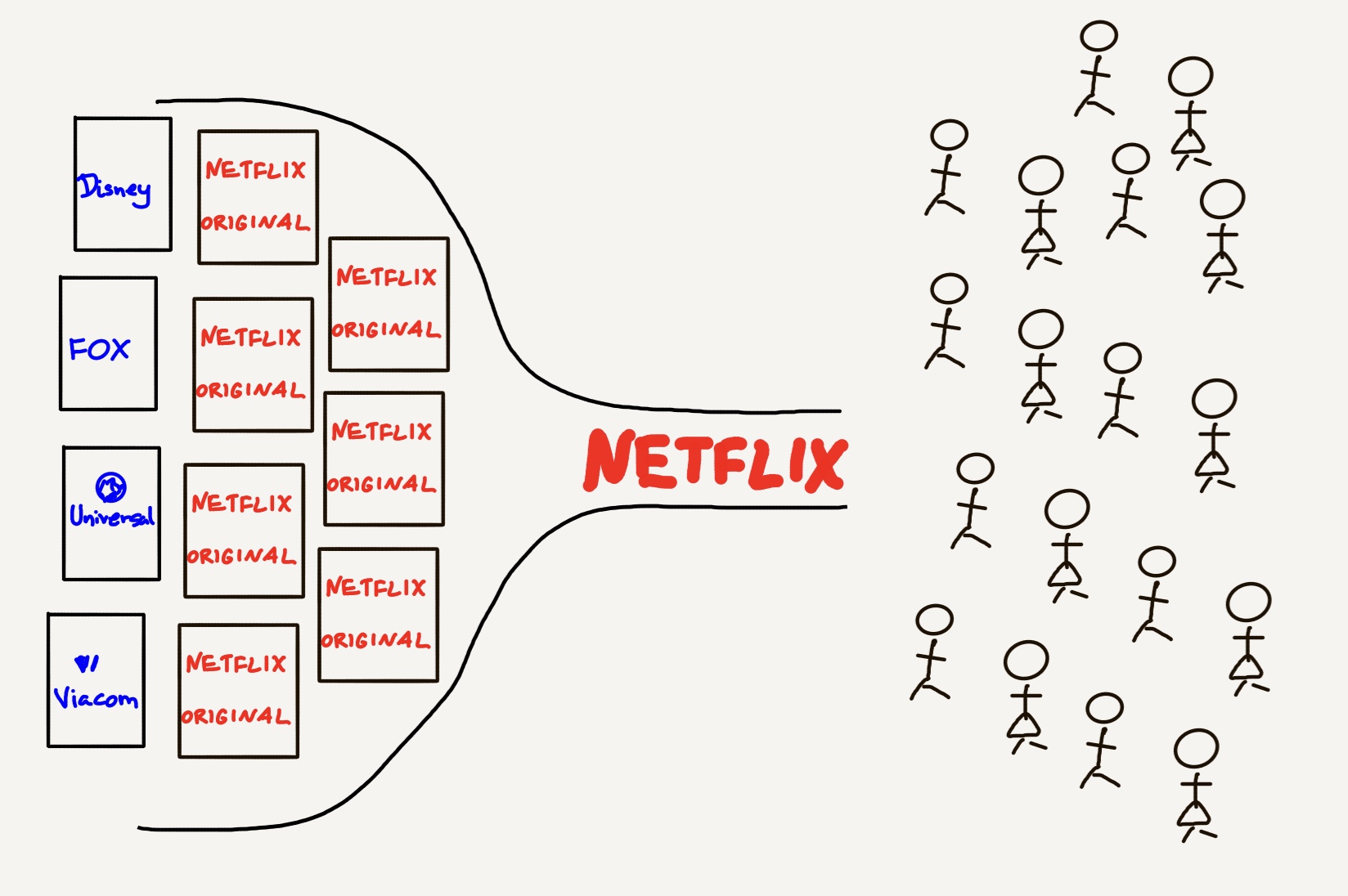

With an increasingly high-profile brand, large user base, and ever deeper pockets, Netflix moved into original programming that was orthogonal to traditional programming buyers: creators had full control and a guarantee that they could create entire seasons at a time

Each of these intermediary steps was a necessary prerequisite to everything that followed, culminating in yesterday’s announcement: Netflix can credibly offer a service worth paying for in any country on Earth, thanks to all of the IP it itself owns. This is how a company accomplishes what, at the beginning, may seem impossible: a series of steps from here to there that build on each other. Moreover, it is not only an impressive accomplishment, it is also a powerful moat; whoever wishes to compete has to follow the same time-consuming process.

Another way to characterize Netflix’s increasing power is Aggregation Theory : Netflix started out by delivering a superior user experience of an existing product (DVDs) to a dedicated set of customers, leveraged that customer base to gain new kinds of supply (streaming content), gaining more customers and more supply, and ultimately leveraged those customers to modularize supply such that the streaming service now makes an increasing amount of its content directly.

What Disney is seeking to prove, though, is that it can compete with Netflix directly by following a very different path.

The Onrushing Future

I’ve long argued that the only way to break away from the power of aggregators is through differentiation; it’s why I argued after that Iger earnings call that Disney would be OK — after all, differentiated content is Disney’s core competency, as demonstrated by its ability to extract profits from cable companies.

The implication of Netflix’s shift to original programming, though, isn’t simply the fact that the streaming company is a full-on competitor for cable TV: it is a competitor for differentiated content as well. That gives Netflix far more leverage over content suppliers like Disney than the cable companies ever had.

Consider the comparison in terms of BATNA (Best Alternative to a Negotiated Agreement): for distributors the alternative to not carrying ESPN was losing a huge number of customers who cared about seeing live sports; that’s not much of an alternative! Netflix, on the other hand, can — and is! — going straight to creators for content that viewers can watch instead of whatever Disney may choose to withhold if Netflix’s price is unsatisfactory. 1 Clearly it’s working: Netflix isn’t simply adding customers, it is raising prices at the same time, the surest sign of market power.

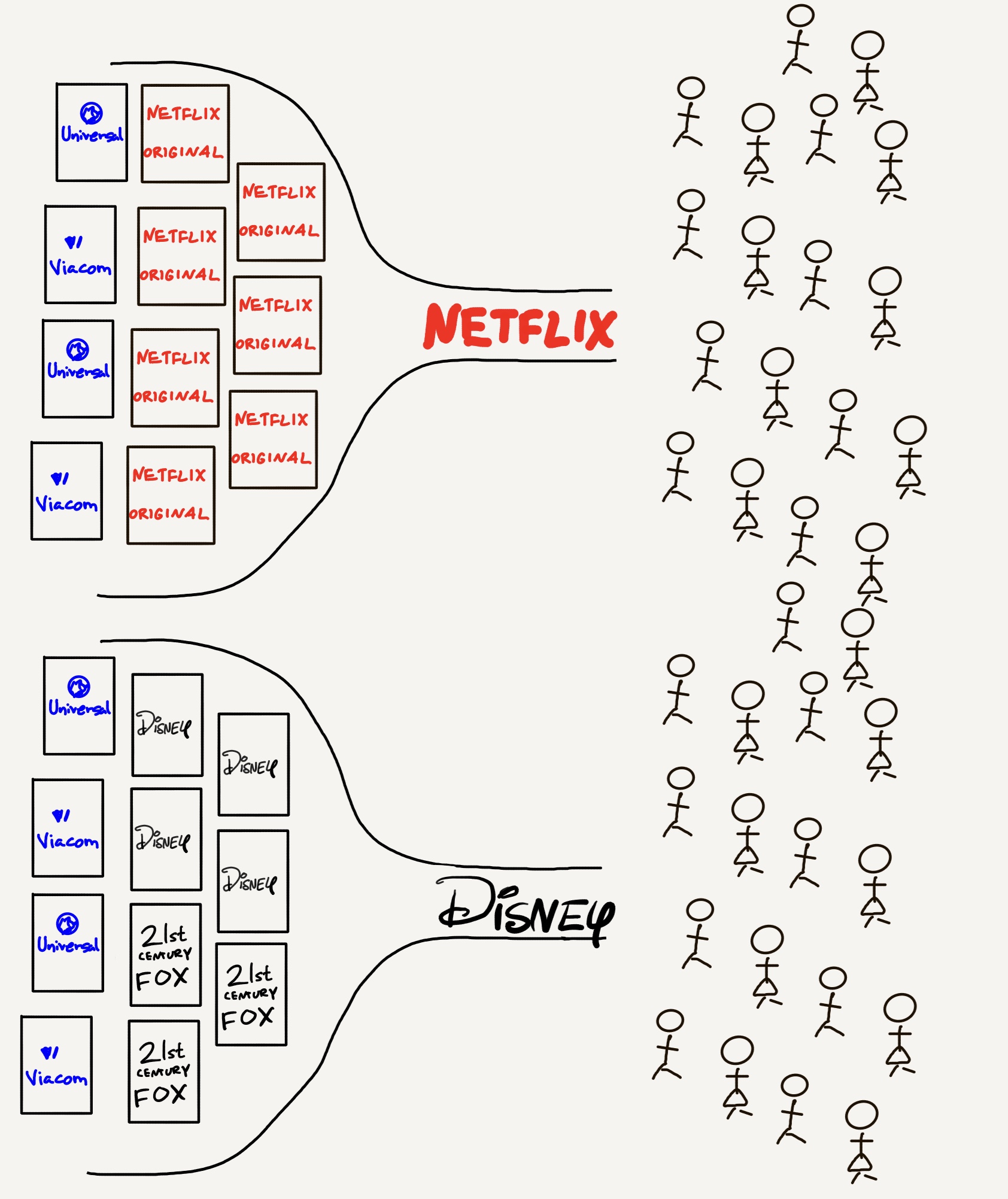

Therefore, the only way for Disney to avoid commoditization is to itself go vertical and connect directly with customers: thus the upcoming streaming service , the removal of its content from Netflix, and, presuming it is announced, this deal. When the acquisition was rumored last month, I wrote in a Daily Update :

This gets at why this deal makes so much sense for Disney. The company already announced that Star Wars and Marvel content would indeed be a part of the streaming service (that is what was still up in the air when I wrote Disney’s Choice ), but the company is absolutely right to not stop there: being a true Netflix competitor means having more content, not less — and that content doesn’t necessarily have to be fresh! Streaming shifted television from a world based on scarcity — there are only 24 hours in the day times however many channels there are, and a channel can only show one thing at a time — to one based on abundance: you can watch anything you want at anytime and it can be different from everyone else.

Moreover, not only does 21st Century Fox have a lot of content, it has content that is particularly great for filling out a streaming library: think The Simpsons, or Family Guy; according to estimates I’ve seen, in terms of external content Fox owns eight of Netflix’s most streamed shows — more than Disney’s six. This content is useful not only for driving sign-ups with certain audiences, but especially for reducing churn; the latter requires a different content strategy than the former.

Whereas Netflix laddered-up to its vertical model and used its power as an aggregator of demand to gain power over supply, Disney is seeking to leverage — and augment — its supply to gain demand. The end result, though, would look awfully similar: a vertically integrated streaming offering that attracts and keeps customers with exclusive content, augmented with licensing deals.

If Disney is successful, it will be a truly remarkable shift: away from a horizontal content company predicated on leveraging its investment in content across as many outlets as possible, to a vertical streaming company that uses its content to achieve higher average revenue from a smaller number of customers willing to pay directly — smaller in the United States, that is; as Netflix is demonstrating, owning it all means the ability to extend the model worldwide. 2

The Antitrust Question

I suspect the final hangup in Disney and 21st Century Fox’s negotiations are termination fees: who pays whom if the deal falls through. There is an obvious reason for concern — antitrust. That, of course, gets at some the reasons (but not all) as to why the deal makes sense in the first place. What is fascinating, though, is that the nature of the concern changes depending on the time frame through which one views this deal.

If one starts with a static view of the world as it is at the end of 2017, then there may be some minor antitrust concerns, but probably nothing that would stop the deal. Disney might have to divest a cable channel or two (the company’s power over distributors would be even stronger; basically the opposite of the some of the concerns that halted the Comcast acquisition of Time Warner), and potentially be limited in its ability to make operational decisions about Hulu (Disney would have a controlling stake after the merger; Comcast was similarly restricted after acquiring NBC Universal, but there the concern was more about Comcast’s conflict of interest with regards to its cable TV business competing with Hulu). The Hulu point is interesting in its own right: Disney could choose to focus its streaming efforts there instead of building its own service, but I suspect it would rather own it all.

In addition, Disney and 21st Century Fox combined for 40% of U.S. box office revenue in 2016 ; that probably isn’t enough to stop the deal, and as silly as it sounds, don’t underestimate the clamoring of fans for the unification of the Marvel Cinematic Universe in swaying popular opinion!

The view changes, though, if you look only a year or two ahead: what I just described above — the “truly remarkable shift” in Disney’s business model — is a shift to vertical foreclosure. The entire point of Disney vastly increasing its content library is to offer that library exclusively on its own streaming service, not competitors’ — especially not on Netflix. Given the current state of antitrust law, which has ignored vertical mergers for years, this would normally be an academic point, except the current state was fundamentally shifted just a few weeks ago, when the Department of Justice sued to block AT&T’s acquisition of Time Warner due to vertical foreclosure concerns.

It’s not a perfect comparison: for one thing, AT&T’s distribution service (DirecTV) already exists, for another, it is impossible to see that acquisition as anything but a vertical one; as I just noted, though, today the Disney-Fox acquisition is a horizontal one. Would the Justice Department sue based on Disney’s potential, as opposed to its reality? And there’s a political angle too: if the AT&T-Time Warner acquisition were indeed blocked as retaliation by the Trump administration against CNN, then it would follow that the administration would be willing to accommodate 21st Century Fox Chairman Rupert Murdoch.

What is most interesting, though, is the long-term view: I have been writing for years that Netflix’s status as an aggregator was positioning the company to dominate entertainment, and it was only eight months ago that I despaired of Disney and the other entertainment companies ever figuring out how to fight back. What has been so impressive over the last few months is the extent and speed with which Disney has seemingly figured it out — and acted accordingly.

Is that a bad thing? Note how much the situation changed once Netflix became a viable competitor for cable TV: competition is a wonderful thing, most of all for consumers. To that end, might it be better for consumers, not-so-much today but ten years from now, if Disney were fully empowered to compete with Netflix? What is preferable? A dominant streaming company and a collection of content companies trying to escape the commoditization trap, or two dominant streaming companies that can at least try to hold each other accountable?

It’s not a great choice, to be honest; certainly Amazon Prime Video is a possible competitor, although the service is both empowered by its business model and also held back . Other tech companies are making noises in the area, but more tech company dominance hardly seems like an answer!

Frankly, I’m not sure of the answer: I am both innately suspicious of these huge mergers and also sympathetic because I see so clearly the centralizing power of the Internet. The big are combining because the giants are coming: if anything, they are already here.

- The primary reason Netflix doesn’t have sports content is because it is not evergreen and thus doesn’t provide a cumulative advantage in terms of lowering customer acquisition costs over time; however, not being subject to the one-sided negotiations inherent to sports rights is a nice side benefit [ ↩ ]

- Just as interesting is the prospective acquisition of regional sports networks and what that means for the future for ESPN; I will discuss this on tomorrow’s Daily Update [ ↩ ]

文章版权归原作者所有。