Amazon Health

Amazon Health

It’s pretty rare for the same company to feature in two consecutive Weekly Articles; yesterday’s announcement of a health care initiative involving Amazon, though, is not only incredibly intriguing, it also fits directly into some of the most important themes on Stratechery. I couldn’t resist.

The Announcement

From a joint press release :

Amazon, Berkshire Hathaway and JPMorgan Chase & Co. announced today that they are partnering on ways to address healthcare for their U.S. employees, with the aim of improving employee satisfaction and reducing costs. The three companies, which bring their scale and complementary expertise to this long-term effort, will pursue this objective through an independent company that is free from profit-making incentives and constraints. The initial focus of the new company will be on technology solutions that will provide U.S. employees and their families with simplified, high-quality and transparent healthcare at a reasonable cost.

Tackling the enormous challenges of healthcare and harnessing its full benefits are among the greatest issues facing society today. By bringing together three of the world’s leading organizations into this new and innovative construct, the group hopes to draw on its combined capabilities and resources to take a fresh approach to these critical matters…

The effort announced today is in its early planning stages, with the initial formation of the company jointly spearheaded by Todd Combs, an investment officer of Berkshire Hathaway; Marvelle Sullivan Berchtold, a Managing Director of JPMorgan Chase; and Beth Galetti, a Senior Vice President at Amazon. The longer-term management team, headquarters location and key operational details will be communicated in due course.

I’ve gotten more and more questions from readers about the possibilities of Amazon and health care, even before this announcement. I’ve been surprised, to be honest, but perhaps I shouldn’t be: I was the one who declared on The Bill Simmons Podcast that “Amazon’s goal is to basically take a skim off of all economic activity”, and given that health care was 17.9% of GDP in 2016, well, I guess that means I predicted this!

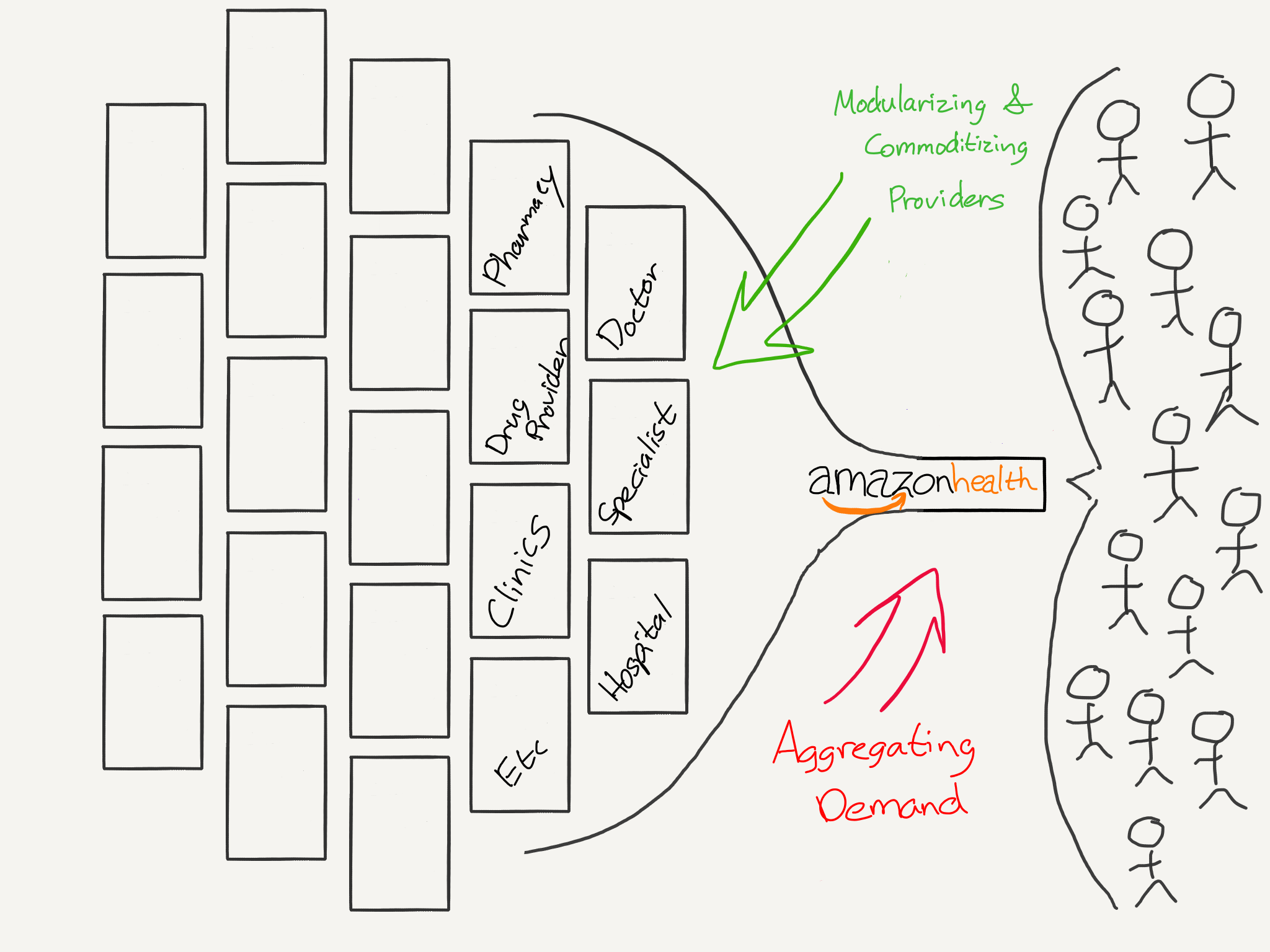

Amazon Health Marketplace

What is “this”, though? It certainly is tempting to jump immediately to a possible end game predicated on the ideas I have laid out in The Amazon Tax , Amazon’s New Customer , and Amazon Go and the Future :

- Amazon builds out “interfaces” for its employees (as well as those of Berkshire Hathaway and J.P. Morgan Chase — I’ll just refer to Amazon from here on out), both digital and physical, to access basic healthcare needs; these sit in front of pharmacy benefit managers (PBMs), insurance administrators, wholesale distributors and pharmacies.

- Amazon starts building out infrastructure for those healthcare suppliers, requiring them to serve Amazon’s employees using a standard interface.

Amazon could then go in one of two directions. First, Amazon could start to backwards integrate into its suppliers’ business; there are hints the company is already exploring pharmaceutical sales , and the Wall Street Journal says the idea was broached. That said, I actually think this is less likely; insurance operates best at more scale, not less: first and foremost, the larger the pool, the more risk can be spread, as well as obvious efficiency gains in administration. More scale also gives more bargaining power over other parts of the healthcare chain. Three companies, large though they may be, aren’t going to be as effective as large insurers, no matter how well-managed they may be.

What would make more sense to me is that, having first built an interface for its employees, and then a standardized infrastructure for its health care suppliers, is that Amazon converts the latter into a marketplace where PBMs, insurance administrators, distributors, and pharmacies have to compete to serve employees. And then, once that marketplace is functioning, Amazon will open the floodgates on the demand side, offering that standard interface to every large employer in America.

Aggregation and Suppliers

This is certainly ambitious enough — basically intermediating U.S. employers and the U.S. healthcare industry — but in fact this only sets the stage for the wholesale disruption of American healthcare. First, Amazon could not only open up its standard interface to other large employers, but small-and-medium sized businesses, and even individuals; in this way the Amazon Health Marketplace could aggregate by far the most demand for healthcare.

Consolidating demand by offering a superior user experience is how aggregators gain power; given the scenario I just sketched out, Aggregation Theory has a prediction about what might happen next:

Once an aggregator has gained some number of end users, suppliers will come onto the aggregator’s platform on the aggregator’s terms, effectively commoditizing and modularizing themselves. Those additional suppliers then make the aggregator more attractive to more users, which in turn draws more suppliers, in a virtuous cycle.

This means that for aggregators, customer acquisition costs decrease over time; marginal customers are attracted to the platform by virtue of the increasing number of suppliers. This further means that aggregators enjoy winner-take-all effects: since the value of an aggregator to end users is continually increasing it is exceedingly difficult for competitors to take away users or win new ones.

The key words there are “commoditize and modularize”, and this is where the option I dismissed above comes into play, but not in the way most think: Amazon doesn’t create an insurance company to compete with other insurance companies (or the other pieces of healthcare infrastructure); rather, Amazon makes it possible — and desirable — for individual health care providers to come onto their platform directly, be that doctors, hospitals, pharmacies, etc.

After all, if Amazon is facilitating the connection to patients, what is the point of having another intermediary? Moreover, by virtue of being the new middleman, Amazon has the unique ability to consolidate patient data in a way that is not only of massive benefit to patients and doctors but also to the application of machine learning.

Of course that leaves the insurance piece, which makes Berkshire Hathaway a useful partner; conveniently, Berkshire Hathaway is not in the health insurance business, but rather the health reinsurance business — that is, they insure the insurers. Or, to put it another way, they don’t provide any of the services that Amazon Health Marketplace might make obsolete, and specialize in the one thing Amazon Health Services would need.

Oh, and this will be really expensive, and take years to get off the ground. It certainly would be helpful to have access to financing and capital markets, which means it would be very helpful to partner with JPMorgan Chase & Company. The skills these three companies bring to bear seems far more relevant than the number of employees (and besides, the company alliance approach to traditional health care has been done ).

Is This Happening?

Needless to say, what I just sketched out is extremely ambitious; it is easy to let one’s mind run wild when it comes to a company without a name, a management team, or a location. Moreover, the press release was quite modest in its ambitions; I quoted it above, but here is the relevant piece again:

The three companies, which bring their scale and complementary expertise to this long-term effort, will pursue this objective through an independent company that is free from profit-making incentives and constraints. The initial focus of the new company will be on technology solutions that will provide U.S. employees and their families with simplified, high-quality and transparent healthcare at a reasonable cost.

Ah yes, “technology solutions”. We’ve certainly seen that before , and it hasn’t worked.

That, though, is where the previous line comes in: the scenario that I sketched out above is wildly profitable, to be sure, but only years down the road when demand is fully aggregated and Amazon Health Marketplace is taking a skim off of every transaction; if short-term profit isn’t the goal, long-term goals become much more realistic.

And there it is, in the first sentence: “this long-term effort.” These three companies are clear up-front that this isn’t a one-off effort; there is the commitment to the long-term, and while “technological solutions” seems like a short-term play, I just explained why that is the place the start. Aggregators win with products that are simple, high-quality, and easy to understand — exactly what this press release promised.

Is This Possible?

I’m not a healthcare expert by any means; I know enough to know that the U.S. system is incredibly complex, bedeviled by incentive problems, and tied up in all kinds of messy ways with regulations (mostly justified!).

At the same time, the U.S. healthcare system is inextricably tied up with the post-World War 2 order; indeed, the entire reason employers are so important to the system is because of World War 2 regulations that instituted price controls on wages, incentivizing employers to use benefits as a means of attracting workers (this was further enshrined by making healthcare benefits tax-exempt).

That system, though, is under more duress than ever. I wrote in TV Advertising’s Surprising Strength — and Inevitable Fall :

What should be terrifying to television executives is that all of those pieces that make television advertising the gold mine that it has been are under the exact same threat that TV watching itself is: the threat of the Internet. Start with the top 25 advertisers in the U.S.…

Notice that the vast majority of the industries on on this list are dominated by massive companies that compete on scale and distribution. CPG is the perfect example: building a “house of brands” allows a company like Procter & Gamble to target demographic groups even as they leverage scale to invest in R&D, bring down the cost of products, and most importantly, dominate the distribution channel (i.e. retail shelf space). Said retailers, meanwhile, are huge in their own right, not only so they can match their massive suppliers at the bargaining table but also so they can scale logistics, inventory management, store development, etc. Automobile companies, meanwhile, are not unlike CPG companies: they operate a “house of brands” to serve different demographics while benefitting from scale in production and distribution; the primary difference is that they make money through one large purchase instead of over many smaller purchases over time.

Note [that nearly all] of the companies on this list are threatened by the Internet.

My thesis in that article — repeated in Dollar Shave Club and the Disruption of Everything and The Sports Linchpin — is that the post-World War 2 economic system was deeply intertwined and interdependent, and that the root of everything was control of distribution. The Internet, though, made the distribution of information free, upsetting not just information providers like publishers, but all industries; it follows, then, that to the extent that the current health care system is built on that post-World War 2 order, such is the extent to which it is vulnerable.

That is not to say its collapse is imminent — quite the opposite, in fact. Each seemingly distinct industry, by virtue of being interdependent on others, supports each other. My expectation, then, is not that the Internet methodically disrupts industry after industry in some sort of chronological order, but rather that the entire edifice lasts far longer than technologists think, only to one day collapse far quicker than anyone expected.

The ultimate winners of this shakeout, then, are not only companies that are building businesses predicated on the Internet, but just as importantly, are willing and able to build those businesses with the patience that will be necessary to wait for the old order to collapse, particularly if that collapse happens years or decades after the underlying business models are rotten.

There is no more patient company than Amazon.

文章版权归原作者所有。