Shopify and the Power of Platforms

Shopify and the Power of Platforms

While I am (rightfully) teased about how often I discuss Aggregation Theory , there is a method to my madness, particularly over the last year: more and more attention is being paid to the power wielded by Aggregators like Google and Facebook, but to my mind the language is all wrong.

I discussed this at length last year:

- Tech’s Two Philosophies highlighted how Facebook and Google want to do things for you; Microsoft and Apple were about helping you do things better.

- The Moat Map discussed the relationship between network effects and supplier differentiation: the more that network effects were internalized the more suppliers were commoditized, and the more that network effects were externalized the more suppliers were differentiated.

- Finally, The Bill Gates Line formally defined the difference between Aggregators and Platforms. This is the key paragraph:

</br>This is ultimately the most important distinction between platforms and Aggregators: platforms are powerful because they facilitate a relationship between 3rd-party suppliers and end users; Aggregators, on the other hand, intermediate and control it.

It follows, then, that debates around companies like Google that use the word “platform” and, unsurprisingly, draw comparisons to Microsoft twenty years ago, misunderstand what is happening and, inevitably, result in prescriptions that would exacerbate problems that exist instead of solving them.

There is, though, another reason to understand the difference between platforms and Aggregators: platforms are Aggregators’ most effective competition.

Amazon’s Bifurcation

Earlier this week I wrote about Walmart’s failure to compete with Amazon head-on ; after years of trying to leverage its stores in e-commerce, Walmart realized that Amazon was winning because e-commerce required a fundamentally different value chain than retail stores. The point of my Daily Update was that the proper response to that recognition was not to try to imitate Amazon, but rather to focus on areas where the stores actually were an advantage, like groceries , but it’s worth understanding exactly why attacking Amazon head-on was a losing proposition.

When Amazon started, the company followed a traditional retail model, just online. That is, Amazon bought products at wholesale, then sold them to customers:

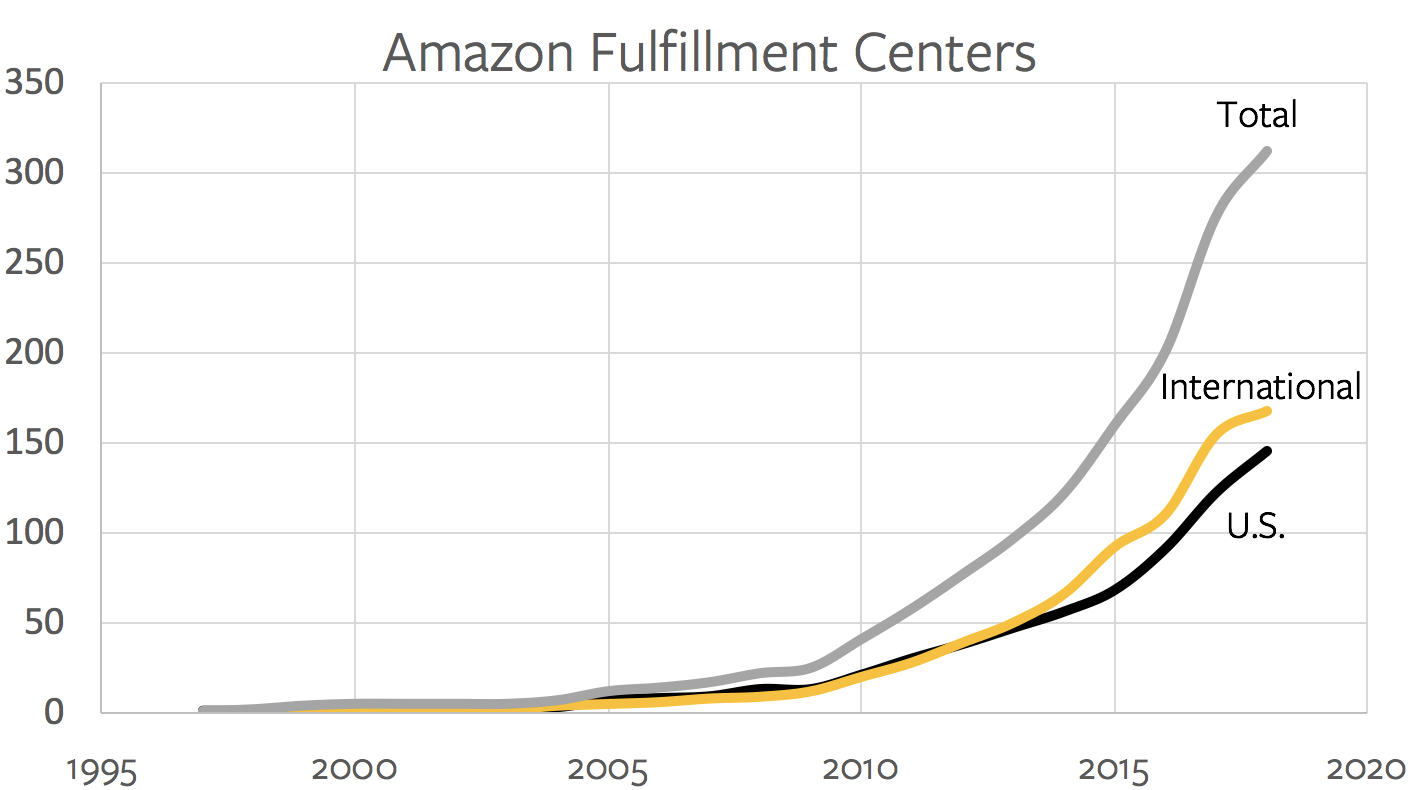

Amazon’s sales proceeded to grow rapidly, not just of books, but also in other media products with large selections like DVDs and CDs that benefitted from Amazon’s effectively unlimited shelf-space. This growth allowed Amazon to build out its fulfillment network, and by 1999 the company had seven fulfillment centers across the U.S. and three more in Europe.

Ten may not seem like a lot — Amazon has well over 300 fulfillment centers today, plus many more distribution and sortation centers — but for reference Walmart has only 20. In other words, at least when it came to fulfillment centers, Amazon was halfway to Walmart’s current scale 20 years ago.

It would ultimately take Amazon another nine years to reach twenty fulfillment centers (this was the time for Walmart to respond), but in the meantime came a critical announcement that changed what those fulfillment centers represented. In 2006 Amazon announced Fulfillment by Amazon , wherein 3rd-party merchants could use those fulfillment centers too. Their products would not only be listed on Amazon.com, they would also be held, packaged, and shipped by Amazon.

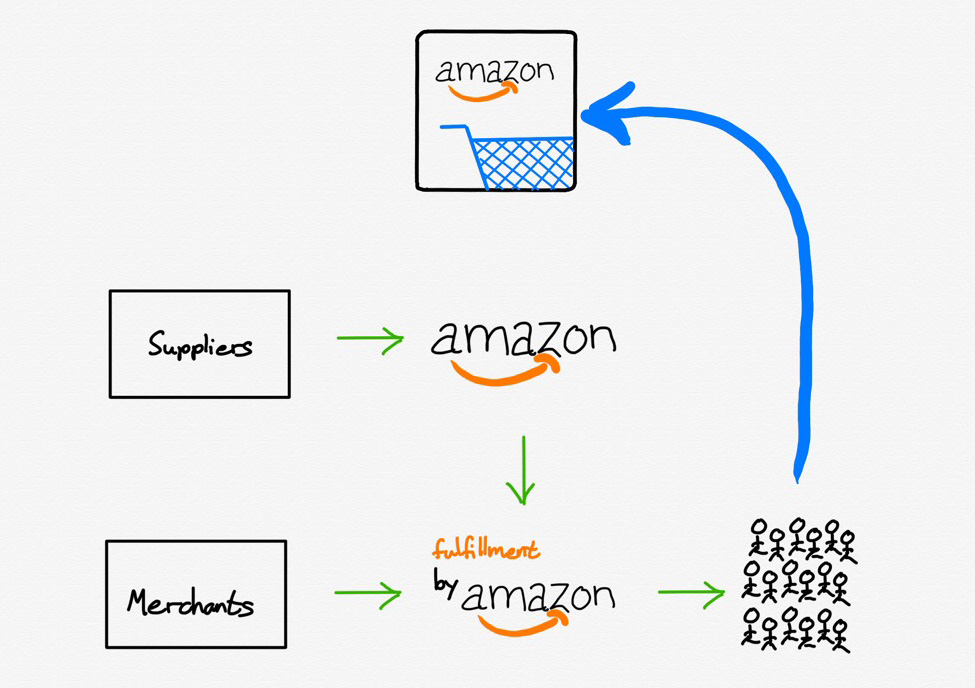

In short, Amazon.com effectively bifurcated itself into a retail unit and a fulfillment unit:

The old value chain is still there — nearly half of the products on Amazon.com are still bought by Amazon at wholesale and sold to customers — but 3rd parties can sell directly to consumers as well, bypassing Amazon’s retail arm and leveraging only Amazon’s fulfillment arm, which was growing rapidly:

Walmart and its 20 distribution centers don’t stand a chance, particularly since catching up means competing for consumers not only with Amazon but with all of those 3rd-party merchants filling up all of those fulfillment centers.

Amazon and Aggregation

There is one more critical part of the drawing I made above:

Despite the fact that Amazon had effectively split itself in two in order to incorporate 3rd-party merchants, this division is barely noticeable to customers. They still go to Amazon.com, they still use the same shopping cart, they still get the boxes with the smile logo. Basically, Amazon has managed to incorporate 3rd-party merchants while still owning the entire experience from an end-user perspective.

This should sound familiar: as I noted at the top, Aggregators tend to internalize their network effects and commoditize their suppliers, which is exactly what Amazon has done. 1 Amazon benefits from more 3rd-party merchants being on its platform because it can offer more products to consumers and justify the buildout of that extensive fulfillment network; 3rd-party merchants are mostly reduced to competing on price.

That, though, suggests there is a platform alternative — that is, a company that succeeds by enabling its suppliers to differentiate and externalizing network effects to create a mutually beneficial ecosystem. That alternative is Shopify.

The Shopify Platform

At first glance, Shopify isn’t an Amazon competitor at all: after all, there is nothing to buy on Shopify.com. And yet, there were 218 million people that bought products from Shopify without even knowing the company existed.

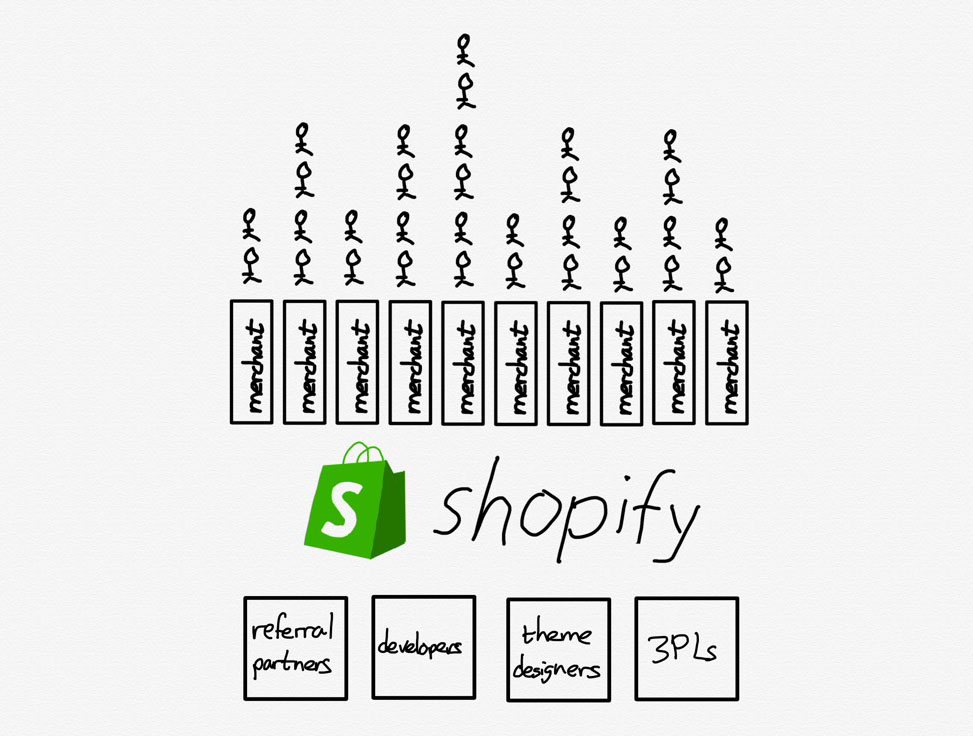

The difference is that Shopify is a platform: instead of interfacing with customers directly, 820,000 3rd-party merchants sit on top of Shopify and are responsible for acquiring all of those customers on their own.

This means they have to stand out not in a search result on Amazon.com, or simply offer the lowest price, but rather earn customers’ attention through differentiated product, social media advertising, etc. Many, to be sure, will fail at this: Shopify does not break out merchant churn specifically, but it is almost certainly extremely high.

That, though, is the point.

Unlike Walmart, currently weighing whether to spend additional billions after the billions it has already spent trying to attack Amazon head-on, with a binary outcome of success or failure, Shopify is massively diversified. That is the beauty of being a platform: you succeed (or fail) in the aggregate.

To that end, I would argue that for Shopify a high churn rate is just as much a positive signal as it is a negative one: the easier it is to start an e-commerce business on the platform, the more failures there will be. And, at the same time, the greater likelihood there will be of capturing and supporting successes.

This is how Shopify can both in the long run be the biggest competitor to Amazon even as it is a company that Amazon can’t compete with: Amazon is pursuing customers and bringing suppliers and merchants onto its platform on its own terms; Shopify is giving merchants an opportunity to differentiate themselves while bearing no risk if they fail.

The Shopify Fulfillment Network

This is the context for one of the most interesting announcements from Shopify’s recent partner conference, Shopify Unite. The name should ring familiar: the Shopify Fulfillment Network.

From the company’s blog :

Customers want their online purchases fast, with free shipping. It’s now expected, thanks to the recent standard set by the largest companies in the world. Working with third-party logistics companies can be tedious. And finding a partner that won’t obscure your customer data or hide your brand with packaging is a challenge.

This is why we’re building Shopify Fulfillment Network—a geographically dispersed network of fulfillment centers with smart inventory-allocation technology. We use machine learning to predict the best places to store and ship your products, so they can get to your customers as fast as possible.

We’ve negotiated low rates with a growing network of warehouse and logistic providers, and then passed on those savings to you. We support multiple channels, custom packaging and branding, and returns and exchanges. And it’s all managed in Shopify.

The first paragraph explains why the Shopify Fulfillment Network was a necessary step for Shopify: Amazon may commoditize suppliers, hiding their brand from website to box, but if its offering is truly superior, suppliers don’t have much choice. That was increasingly the case with regards to fulfillment, particularly for the small-scale sellers that are important to Shopify not necessarily for short-term revenue generation but for long-run upside. Amazon was simply easier for merchants and more reliable for customers.

Notice, though, that Shopify is not doing everything on their own: there is an entire world of third-party logistics companies (known as “3PLs”) that offer warehousing and shipping services. What Shopify is doing is what platforms do best: act as an interface between two modularized pieces of a value chain.

On one side are all of Shopify’s hundreds of thousands of merchants: interfacing with all of them on an individual basis is not scalable for those 3PL companies; now, though, they only need to interface with Shopify.

The same benefit applies in the opposite direction: merchants don’t have the means to negotiate with multiple 3PLs such that their inventory is optimally placed to offer fast and inexpensive delivery to customers; worse, the small-scale sellers I discussed above often can’t even get an audience with these logistics companies. Now, though, Shopify customers need only interface with Shopify.

Plaforms Versus Aggregators

Moreover, this is what Shopify has already accomplished when it comes to referral partners (who drive new merchants onto the platform), developers (who build apps for managing Shopify stores) and theme designers (who sell themes to customize the look-and-feel of stores). COO Harley Finkelstein said at Unite :

You’ve often heard me say that we at Shopify want to create more value for your partners than we capture for ourselves, and I find the best way to demonstrate this is by looking at what I call the “Partner Economy”. The “Partner Economy” is the amount of revenue that flows to all of you our partners…in 2018 Shopify made about a billion dollars [ Editor: in revenue ]. We estimate that you, our partners, made more than $1.2 billion.

In other words, Shopify clears the Bill Gates Line — it captures a minority of the value in the ecosystem it has created — and the Shopify Fulfillment Network should fit right in:

What is powerful about this model is that it leverages the best parts of modularity — diversity and competition at different parts of the value chain — and aligns the incentives of all of them. Every referral partner, developer, theme designer, and now 3PL provider is simultaneously incentivized to compete with each other narrowly and ensure that Shopify succeeds broadly, because that means the pie is bigger for everyone.

This is the only way to take on an integrated Aggregator like Amazon: trying to replicate what Amazon has built up over decades, as Walmart has attempted, is madness. Amazon has the advantage in every part of the stack, from more customers to more suppliers to lower fulfillment costs to faster delivery.

The only way out of that competition is differentiation; granted, Walmart has tried buying and launching new brands exclusive to its store, but differentiation when it comes to e-commerce goods doesn’t arise from top down planning. Rather, it bubbles up from widespread opportunity (and churn!), like that created by Shopify, supported by an entire aligned ecosystem.

- While Amazon is not technically an Aggregator — the company deals with physical goods that absolutely have both marginal and transaction costs — one way to understand the company’s dominance is that its massive investments in logistics have driven those costs much lower than its competitors, allowing the company to reap many of the same benefits. [ ↩ ]

文章版权归原作者所有。