At first glance, the proposed (and now-withdrawn) acquisition of Harry’s Razors by Edgewell Personal Care Co. — the makers of Schick — and Intuit’s announced acquisition of Credit Karma don’t appear to have much in common. There is, though, a common thread: digital advertising, and the dominance of Facebook and Google.

FTC Sues to Block Harry’s Acquisition

Start with Harry’s: the acquisition, which was announced last May , is off the table after the FTC filed a suit to block the acquisition. Interestingly, despite the fact that Harry’s is associated with direct-to-consumer (DTC), the reasoning the FTC used was Harry’s presence in brick-and-mortar retail. From the FTC complaint :

Harry’s and Dollar Shave Club quickly succeeded in — and largely filled — the previously untapped online space. But the successful entry by Harry’s and Dollar Shave Club with their online Direct to Consumer (“DTC”) models did not stop the price increases by P&G and Edgewell, both of which sold their products primarily through brick-and-mortar retailers.

Significant change came when Harry’s made the first — and, to date, only — successful jump from an online DTC platform into brick-and-mortar retail. In August 2016, Harry’s launched exclusively at Target with suggested retail prices several dollars below the most comparable Schick and Gillette products, a significant discount. Harry’s arrival in Target made a substantial impact, with Harry’s immediately winning customers from Edgewell and P&G. Edgewell described Harry’s trajectory as one of “[REDACTED]” and observed that Harry’s took “[REDACTED].”

Harry’s entry at Target ended the long-standing practice of reciprocal price increases by Gillette and Edgewell. Shortly after Harry’s successful launch at Target, P&G implemented a “[REDACTED]” price reduction across its portfolio of razors, reversing course on its practice of leading yearly price increases. Edgewell changed course as well, abandoning its strategy of being a “[REDACTED]” of Gillette’s pricing actions. Rather than match Gillette’s price decrease, Edgewell began tracking Harry’s growth and increased promotional spend (funding for discounts and other promotions) [REDACTED]. Edgewell hoped that this effort would “[REDACTED],” [REDACTED].

The FTC went on to note:

Harry’s significant entry into brick-and-mortar retail transformed the wet shave razor market from a comfortable duopoly to a competitive battleground. Edgewell, in particular, has found itself fighting the threat that Harry’s poses to both its branded products and its private label offerings (i.e., razors manufactured by Edgewell for a retailer partner, to be sold under the retailer’s brand). Consumers benefited from the resulting price discounts and the introduction of additional Edgewell branded and private label choices.

The Proposed Acquisition is likely to result in significant harm by eliminating competition between important head-to-head competitors. The Proposed Acquisition also will harm competition by removing a particularly disruptive competitor from the marketplace at a time when that competitor is currently expanding into additional retailers.

Finally, the FTC concluded that the acquisition was presumptively illegal using the Herfindahl-Hirschman Index , which measures concentration in a given market:

Under the 2010 U.S. Department of Justice and Federal Trade Commission Horizontal Merger Guidelines (“Merger Guidelines”), a post-acquisition market concentration level above 2,500 points, as measured by the Herfindahl-Hirschman Index (“HHI”), and an increase in HHI of more than 200 points renders an acquisition presumptively unlawful. Transactions in highly concentrated markets—markets with an HHI above 2,500 points — with an HHI increase of more than 100 points potentially raise significant competitive concerns and warrant scrutiny. The HHI is calculated by totaling the squares of the market shares of every firm in the relevant market pre- and post-acquisition.

The market for the manufacture and sale of wet shave razors in the United States is already highly concentrated, with an HHI of over 3,000. The Proposed Acquisition increases the concentration in this market by more than 200 points and is therefore presumptively illegal…Changes in HHI based on current market shares understate the competitive significance of the Proposed Acquisition because Harry’s continues to expand into additional brick-and-mortar retailers. Recognizing that the Proposed Acquisition will arrest Harry’s independent expansion, it is appropriate to analyze Harry’s competitive significance by using prior entry events to project future competitive significance. Moreover, current market shares especially understate the competitive significance of Harry’s in markets that include sales of women’s razors because Harry’s Flamingo product launched very recently.

Schick abandoned the deal a few days after the FTC filed suit; Harry’s, surprisingly, did not negotiate a breakup fee.

Acquisitions and Incentives

I quoted fairly extensively from the FTC’s complaint because, frankly, it’s quite compelling. Harry’s emergence led to lower prices for consumers, and Edgewell was almost certainly looking to relieve said downward pressure on prices, along with other more upstanding motivations like gaining new management expertise and its own DTC channel.

At the same time, you can see some of the problematic incentives inherent in blocking a merger that I discussed two weeks ago . First, given that most CPG categories are dominated by a small number of incumbents (given the scale advantages necessary to compete for shelf space globally), investors have to be increasingly wary of investing in the space given that the precedent is that an acquisition will be ruled to be anticompetitive; much will rest on Harry’s ability to fulfill the FTC’s faith in its ability to be a standalone competitor (of which I am dubious, for reasons I will explain). Second, Harry’s was in some respects punished by its leap from online-only sales to bricks-and-mortar sales; as noted in an excerpt above, Harry’s success in online sales didn’t have any appreciable impact on the bricks-and-mortar market. Is the lesson for other DTC companies to stick with online sales alone for fear of foreclosing the possibility of being acquired?

That drives to a broader question: why did Harry’s feel the need to pursue the brick-and-mortar market at all?

The Conservation of Attractive Consumer Packaged Goods

Much of the excitement around DTC was about the potential of eliminating the middleman; the margin taken by retailers could instead be devoted to a better product, lower prices, and better margins for the brand in question. The problem is that value chain transformation is far more dynamic than that. Go back to The Conservation of Attractive Profits , which I wrote about in the context of Netflix in 2015:

The Law of Conservation of Attractive Profits 1 was first explained by Clayton Christensen in his 2003 book The Innovator’s Solution :

Formally, the law of conservation of attractive profits states that in the value chain there is a requisite juxtaposition of modular and interdependent architectures, and of reciprocal processes of commoditization and de-commoditization, commoditization, that exists in order to optimize the performance of what is not good enough. The law states that when modularity and commoditization cause attractive profits to disappear at one stage in the value chain, the opportunity to earn attractive profits with proprietary products will usually emerge at an adjacent stage.

That’s a bit of a mouthful, but the example that follows in the book shows how powerful this observation is:

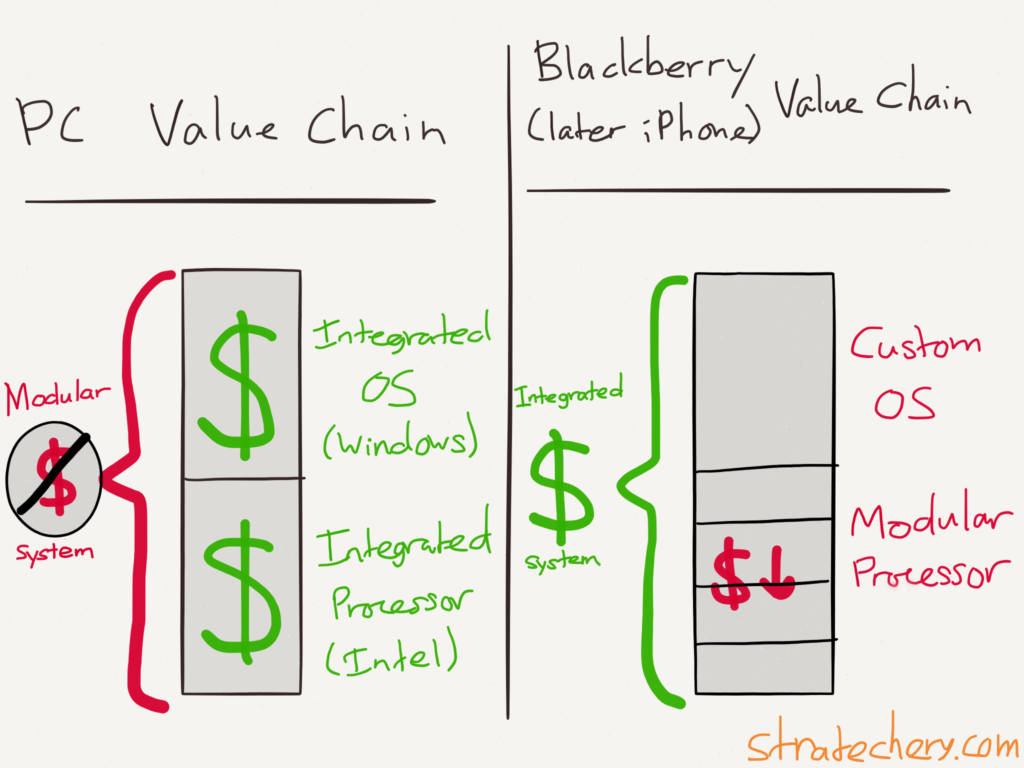

If you think about it in a hardware context, because historically the microprocessor had not been good enough, then its architecture inside was proprietary and optimized and that meant that the computer’s architecture had to be modular and conformable to allow the microprocessor to be optimized. But in a little hand held device like the RIM BlackBerry, it’s the device itself that’s not good enough, and you therefore cannot have a one-size-fits-all Intel processor inside of a BlackBerry, but instead, the processor itself has to be modular and conformable so that it has on it only the functionality that the BlackBerry needs and none of the functionality that it doesn’t need. So again, one side or the other needs to be modular and conformable to optimize what’s not good enough.

Did you catch that? That was Christensen, a full four years before the iPhone, explaining why it was that Intel was doomed in mobile even as ARM would become ascendent. 2 When the basis of competition changed away from pure processor performance to a low-power

system

the chip architecture needed to switch from being integrated (Intel) to being modular (ARM), the latter enabling an integrated BlackBerry then, and an integrated iPhone four years later. 3

The PC is a modular system whose integrated parts earn all the profit. Blackberry (and later iPhones) on the other hand was an integrated system that used modular pieces. Do note that this is a drastically simplified illustration.

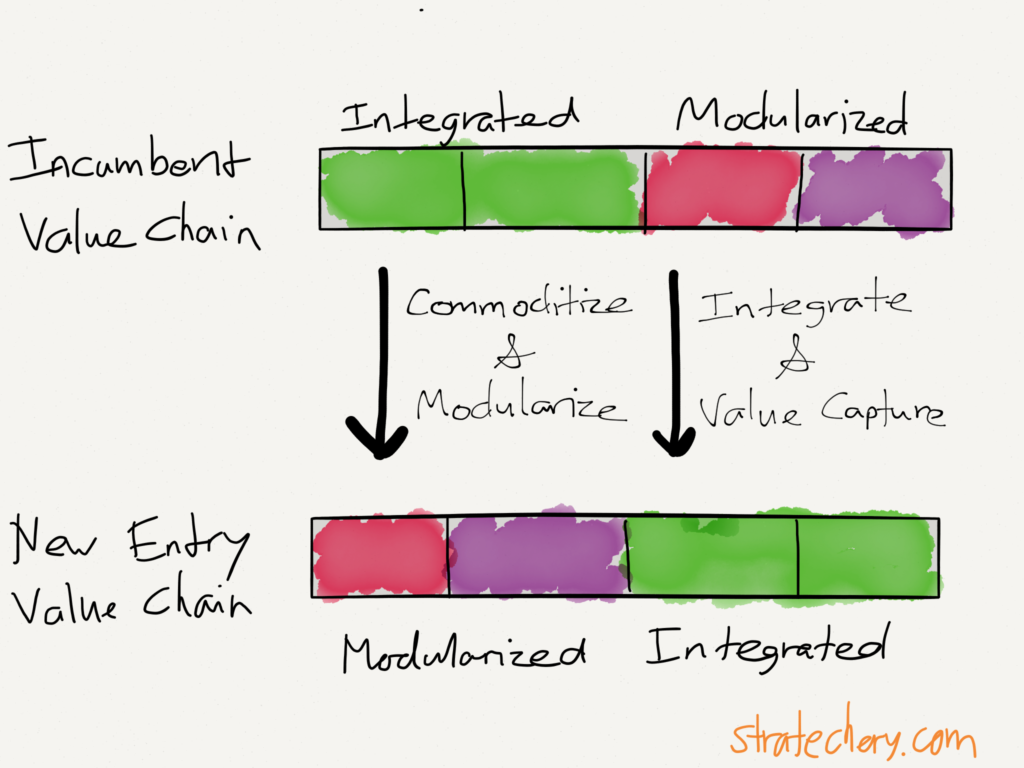

More broadly, breaking up a formerly integrated system — commoditizing and modularizing it — destroys incumbent value while simultaneously allowing a new entrant to integrate a different part of the value chain and thus capture new value.

Commoditizing an incumbent’s integration allows a new entrant to create new integrations — and profit — elsewhere in the value chain.

This is exactly what is happening with Airbnb, Uber, and Netflix too.

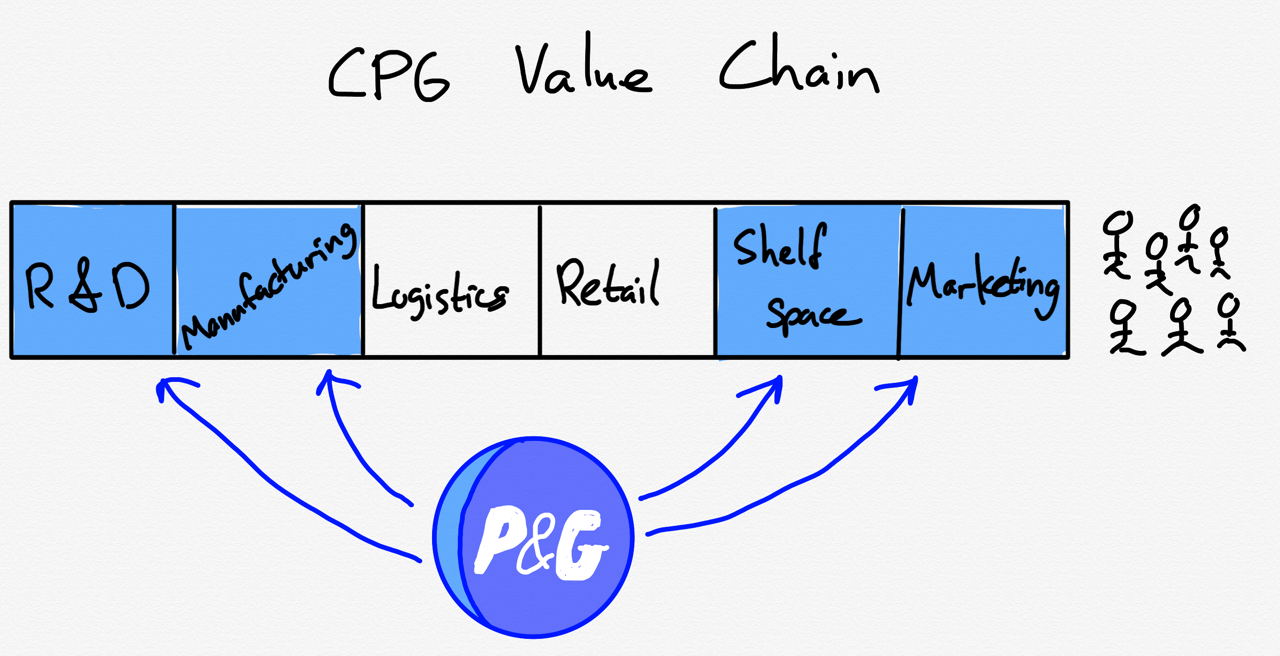

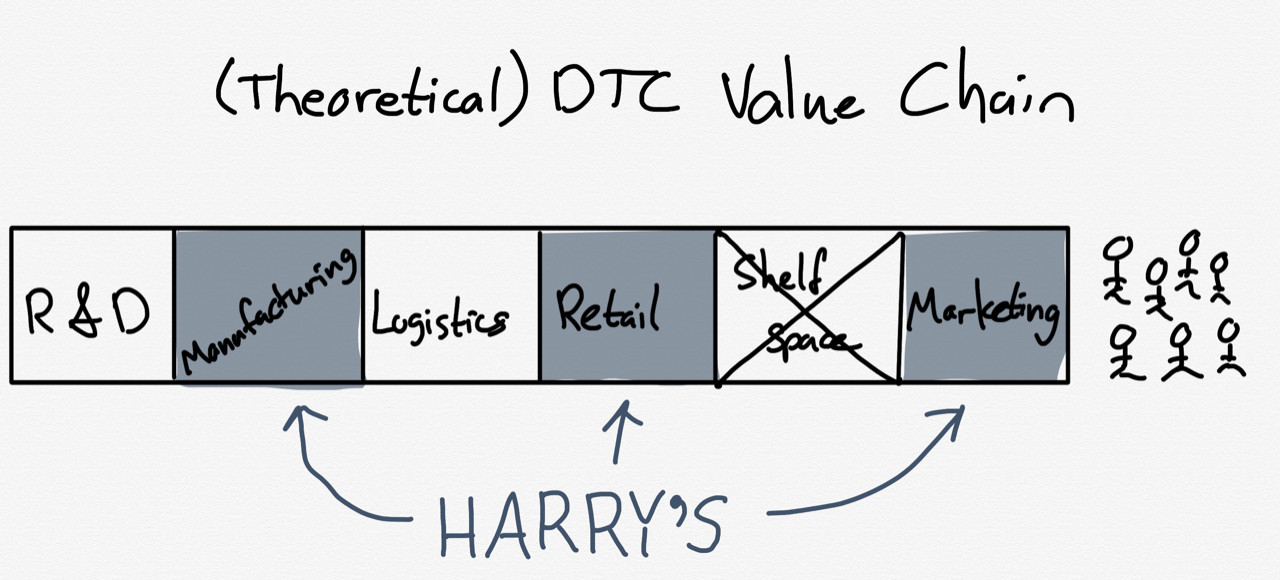

The old value chain in consumer packaged goods (CPG) looked like this:

CPG companies like P&G harvested most of the value by integrating research and development, manufacturing, marketing, and shelf space; raw materials, retail, and logistics were modularized and commoditized.

DTC companies, meanwhile, saw research and development as increasingly unnecessary in overserved markets (as I noted in the context of Dollar Shave Club , razors are a particularly salient example of overserving), and shelf space on the Internet was effectively infinite. Their goal was to integrate marketing, retail, and manufacturing:

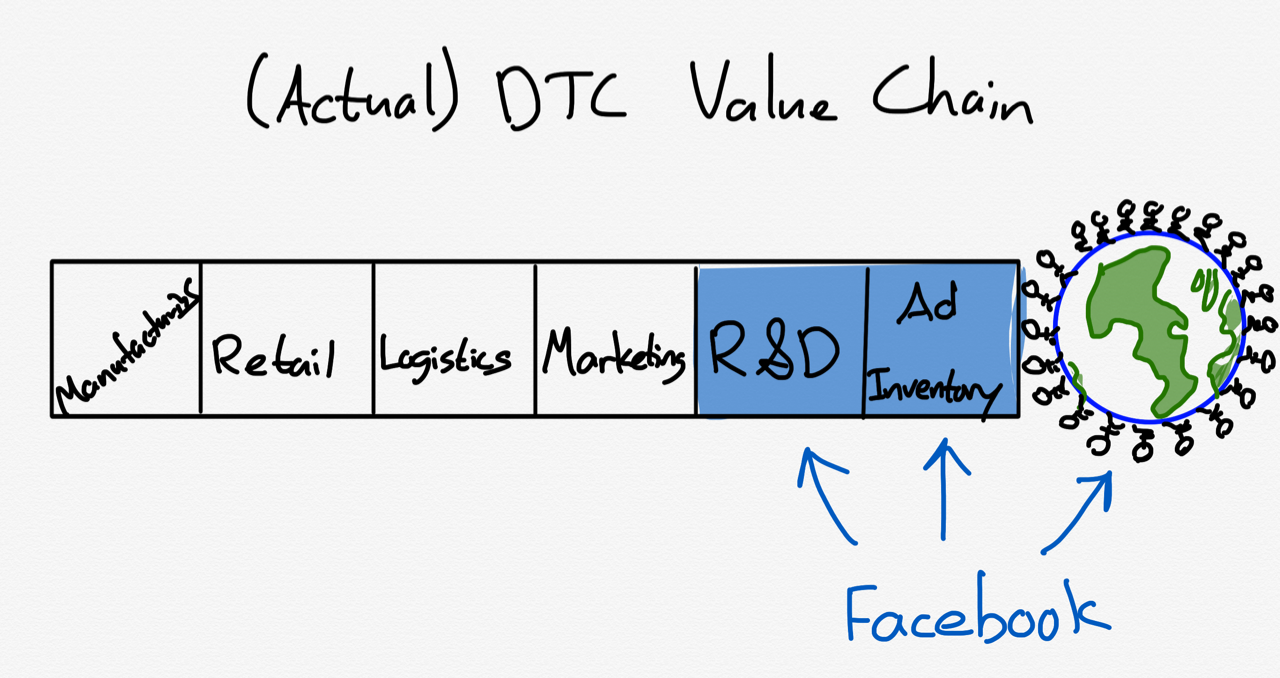

The problem, though, is that marketing on the Internet was entirely different than the analog marketing that previously dominated the CPG industry. There being good at advertising, whether it be coupons in the Sunday paper or television ads during the evening news, was mostly a matter of the abiltiy to spend, which was itself a matter of scale . Digital marketing, though, didn’t really work at scale, at least relative to TV; in fact, it only made sense if you could target consumers with advertising and track how it performed.

On one hand, this was another critical factor in making DTC companies viable. The advantage of targeted advertising is that it takes a lot less money relative to TV to reach customers who are actually interested in your product; the problem, though, is that getting good at targeted advertising requires massive amounts of both research and development to buid the capability, and inventory across a sufficiently large customer base to make the effort worthwhile. In the end, no DTC company was actually good at marketing; they outsourced it to Google and Facebook, which both had the inventory and the capability to spend the billions necessary to develop sophisticated targeted advertising.

The problem is that in the process of depending on Google and Facebook for marketing, the DTC companies gave up their planned integration in the value chain, and the associated profits, to Facebook and Google:

The actual integrated players — Google and Facebook — integrate customers and research and development to dominate marketing; DTC may have online retail operations, but that is a modularized — and thus commoditized — part of the value chain (and meanwhile, Amazon was in the process of integrating retail and logistics). I wrote last week when Brandless folded :

Here is the problem for DTC companies: Facebook really is better at finding them customers than anyone else. That means that the best return-on-investment for acquiring customers is on Facebook, where DTC companies are competing against all of the other DTC companies and mobile game developers and incumbent CPG companies and everyone else for user attention. That means the real winner is Facebook, while DTC companies are slowly choked by ever-increasing customer acquisition costs. Facebook is the company that makes the space work, and so it is only natural that Facebook is harvesting most of the profitability from the DTC value chain.

To be fair to the DTC companies, they are hardly the first to make this mistake: way back when the world wide web first started publishers looked at the Internet and only saw the potential of reaching new customers; they didn’t consider that because every other publisher in the world could now reach those exact same customers, the integration that drove their business — publishing and distribution in a unique geographic area — had disintegrated. It is a lesson that can be taken broadly: if some part of the value chain becomes free, that is not simply an opportunity but also a warning that the entire value chain is going to be transformed.

Harry’s Difficult Road

This takes us back to Harry’s, and the decision to pursue bricks-and-mortar retail in the first place. It’s a choice that doesn’t make much sense in the theoretical value chain I sketched out above, where DTC companies integrate marketing and retail. However, once it became apparent that Facebook and Google squeezed far more value out of the online value chain than offline, the only option left was to pursue some sort of low-end disruption in the old value chain. Or, to put it in blunter terms, be cheaper.

This, though, resulted in two problems: first, there was no technologically-based reason that Harry’s razors should be cheaper than Schick’s or Gillette’s; that meant that Schick and Gillette responded by lowering prices to match Harry’s. Secondly, because price as a proxy for consumer welfare is the most important factor driving regulatory review of acquisitions, Harry’s actually closed off their most viable exit. The fact of the matter is that Schick and Gillette specifically, and large CPG companies broadly, are unsurprisingly better suited to compete in the bricks-and-mortar markets they were built to dominate. Harry’s, despite its factory in Germany and omnichannel distribution strategy, faces a long road to actually achieving that $1.37 billion valuation on their own.

Credit Karma and Acquiring Customers

Harry’s outcome seems paritcularly unfair in light of yesterday’s news that Intuit is buying Credit Karma for $7.1 billion . Credit Karma doesn’t have a factory in Germany. Indeed, they don’t make any money from customers at all. Rather, Credit Karma offers free services that attract users to their site, and monetizes those users by directing them to credit cards and other financial products that pay an affiliate fee.

Here there is one angle where this deal looks a bit like Harry’s: one of Credit Karma’s free offerings is a free tax filing service; that is obviously a threat to TurboTax, Intuit’s biggest money-maker (which has a free version it hopes you never find). It is even possible that the FTC seeks to block the deal on these grounds. I suspect, though, that Credit Karma and Intuit will simply agree to spin off the tax filing unit, because that is not Credit Karma’s true value.

What is actually valuable are Credit Karma’s users — 90 million of them in the U.S. alone, 50% of whom are millennials. Those 90 million users don’t just visit Credit Karma directly, they have already shared substantial amounts of their personal financial data, and have consented to receiving emails about their credit scores. They are, in other words, the best possible customer acquisition channel for a company like Intuit, and for all of the reasons I just recounted, customer acquisition is the most valuable part of the digital value chain. Intuit will gladly suffer a tax filing competitor as long as it has the best possible channel to acquire the next generation of tax filers.

This gets at the real commonality between Harry’s and Credit Karma: Harry’s is less valuable than it might have been because of Facebook and Google’s dominance of digital advertising; Credit Karma is more valuable than it might seem because they offer a way to acquire customers without depending on Facebook and Google. This is a particularly notable insight given the FTC’s involvement in the Harry’s acquisition, and potential involvement in Credit Karma: one potential outcome of the greater competition that may have arisen in digital advertising absent Facebook’s acquisition of Instagram and Google’s acquisition of DoubleClick would be increased viability for DTC companies, and decreased value for simply aggregating an audience with no direct business model.

Still, I wouldn’t take the counter-factual too far: DTC makes far more sense with radically lower cost structures ; if you are going to take advantage of the Internet transforming one part of the value chain, you had best ensure you are anticipating the transformations in the other parts as well. And, on the flipside, in a world of abundance being able to aggregate demand is more valuable than being able to create supply; it may offend our analog sensibilities that 90 million email addresses are more valuable than real-world factories, but such is the transformative nature of the Internet.

Later renamed the Law of Conservation of Modularity. [ ↩ ]

As I’ve noted , the iPhone is in fact modular at the component level; the integration is between the completed phone and the software. Not appreciating that the point of integration (or modularity) can be anywhere in the value chain is, I believe, at the root of a lot of mistaken analysis about the iPhone in particular [ ↩ ]